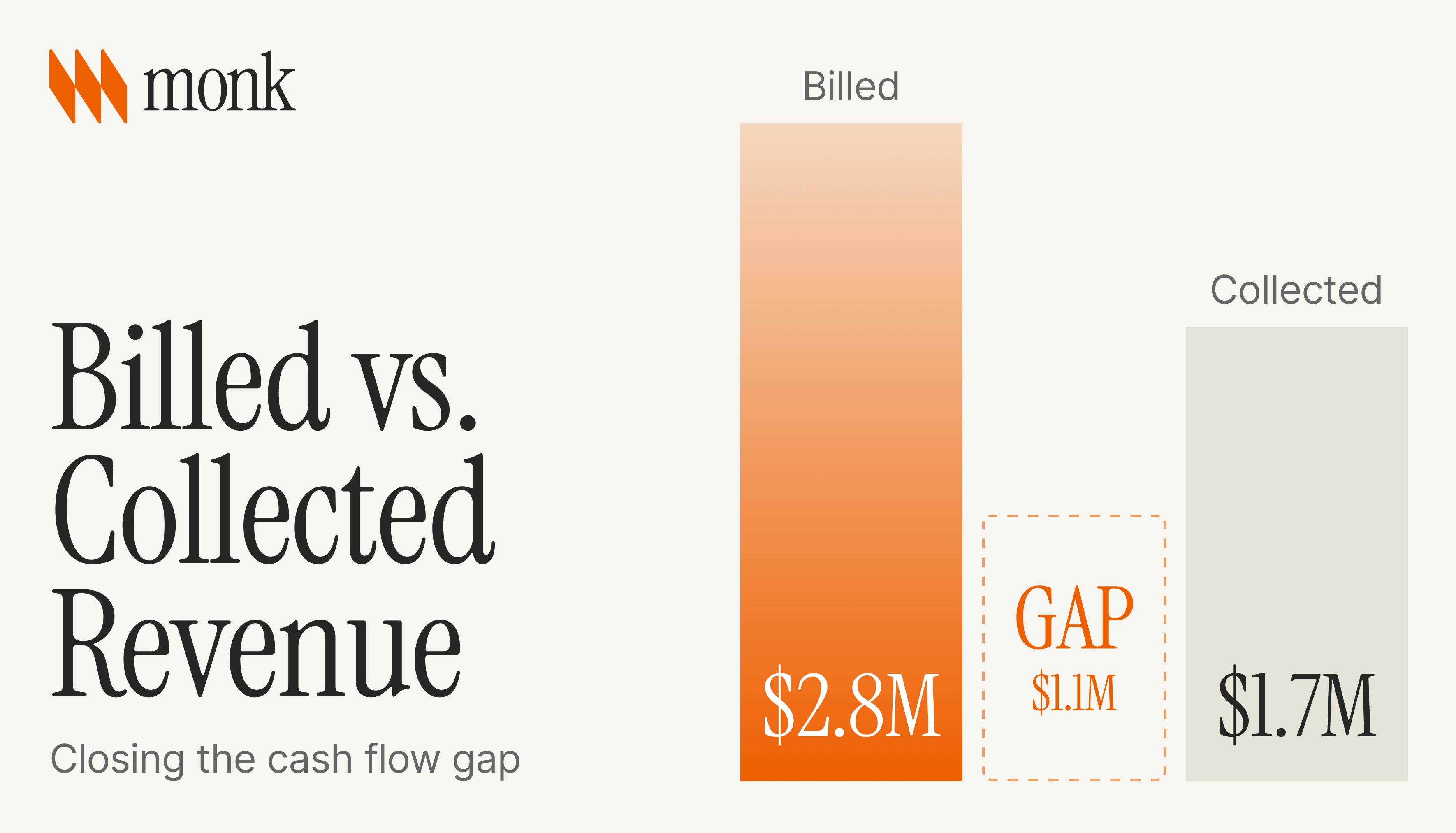

Billed vs. Collected Revenue: Closing the Cash Flow Gap

What Is the Difference Between Billed and Collected Revenue?

Billed revenue is the total value of invoices you have issued, while collected revenue is the cash sitting in your account, and the gap between them is one of the most dangerous blind spots in finance. Under accrual accounting, billed revenue is recognized the moment an invoice goes out, whether the customer pays in 10 days or 10 months. That means a business can show strong revenue growth while struggling to make payroll, because the cash has not arrived yet. Turning billed revenue into collected cash, or at least measuring it accurately, is a survival skill rather than a nicety.

This article explains why the gap exists, how it distorts your cash flow forecast, and how to fix it. Monk attacks the root cause by accelerating collections and applying cash accurately, and for the broader context on the systems involved, our overview of what accounts receivable automation covers is a useful companion.

Why Does the Billed-to-Collected Gap Exist?

The gap exists for structural reasons, not because of poor management. It is built into how B2B commerce works.

Extended payment terms are the most common cause: Net-30, Net-60, and Net-90 mean revenue recognized today may not convert to cash for months. Late payments compound it, since a meaningful share of invoices are paid past terms. Disputes and deductions create a difference between billed and collected when customers short-pay or request credits, and invoice errors legitimately delay payment by restarting the clock until they are resolved. There is also a quieter cause: unapplied cash. When a payment has arrived but has not yet been matched to its invoices, the collected figure understates reality, which is why accurate cash application is part of connecting billed and collected revenue. The hidden cost of that backlog is exactly what we cover in our look at the true cost of poor cash application.

How Does the Gap Distort Your Cash Flow Forecast?

Most forecasts use billed revenue as a proxy for incoming cash, which bakes in a compounding error. The further your collection reality is from your assumption, the worse the forecast.

If your average collection period is 45 days but your forecast assumes 30, you consistently overstate near-term liquidity. Across hundreds of open invoices, that error becomes material, and teams approve hiring, vendor payments, and capital spend against cash that exists only on paper. The danger is that the forecast looks precise even while it is systematically wrong, so no one questions it until a cash crunch makes the gap impossible to ignore. The same unreconciled receivables also slow down the month-end close, since the team has to chase the difference before the books can be finalized. The cruel part is timing: the gap is widest in fast-growing companies, because each month of new billings adds another cohort of receivables that has not yet converted to cash, so the faster you grow, the more cash appears to be missing even when collections are healthy.

What Is DSO and Why Does It Matter?

Days Sales Outstanding quantifies the billed-to-collected gap by measuring the average number of days it takes to collect cash after an invoice is issued. It is the single clearest number for tracking how wide the gap is.

To calculate it, divide your AR balance by total credit sales, then multiply by the days in the period. A rising DSO is an early warning that the gap is widening, and tracking it by customer segment shows whether one large slow payer is masking healthy performance elsewhere. It is also worth watching DSO as a trend rather than a single snapshot, because one slow month can be noise while three in a row is a signal. For finance leaders, DSO is the highest-leverage number to manage, which is why our guide to reducing DSO with six strategies treats it as the central lever for converting billed revenue into collected cash.

How Do You Build a More Accurate Forecast?

The fix is to shift from invoice-date thinking to collection-probability thinking. A good cash forecast models when money will arrive, not when it was billed.

Age your receivables into 0-30, 31-60, 61-90, and 90-plus buckets and apply a realistic collection probability to each, drawn from your own history rather than a generic assumption. Layer in customer-level context, since a customer who always pays on day 45 should be modeled at 45, not 30. Keep your P&L forecast separate from your cash forecast, and model conservative and optimistic scenarios so the range reveals your real liquidity risk. Revisit the probabilities each quarter, because payment behavior shifts with the economy and with your own collections discipline, and a model built on last year's assumptions slowly drifts back toward the same billed-revenue error you were trying to avoid. If your projections keep missing despite this discipline, our breakdown of why AR forecasts are almost always wrong digs into the data problem underneath. The accuracy of all of this depends on a clean ledger, which means cash must be applied correctly and promptly, a discipline covered in our explainer on how remittance matching works.

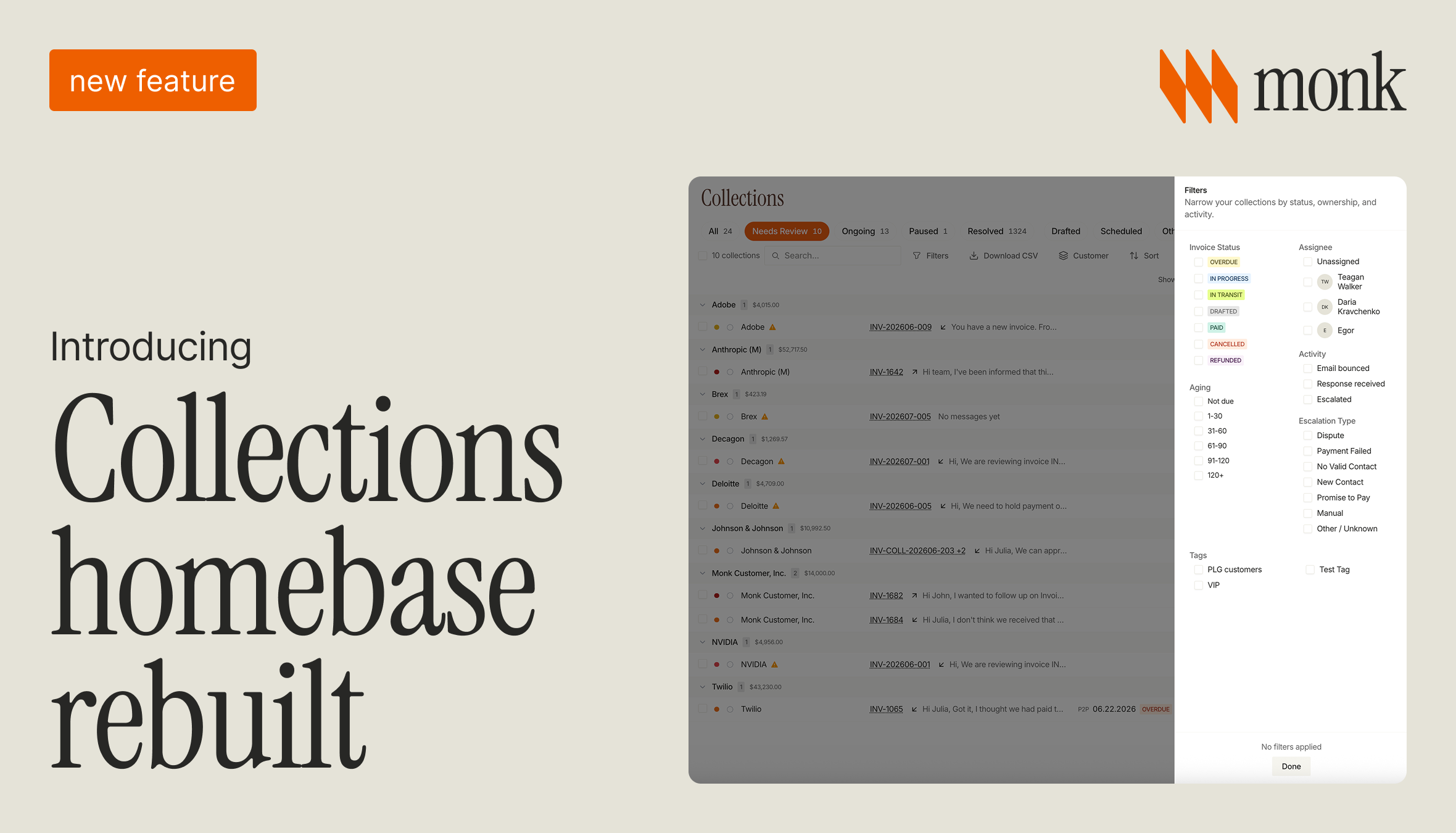

How Does AR Automation Turn Billed Revenue Into Cash?

Manual AR is slow and inconsistent, which is exactly what widens the gap. Automation attacks both the speed and the accuracy of the cycle.

Invoices reach the right contact immediately, and reminders go out consistently without depending on someone remembering. Monk's intelligent collections goes beyond fixed dunning by ingesting the context of prior conversations so outreach reflects each customer's history, which Monk reports is 24% more effective than standard dunning. Getting paid closer to due dates compresses DSO and narrows the billed-to-collected gap, so your forecast reflects something close to your actual cash position. At the same time, AI-native cash application matches incoming payments at an 80% automatic match rate, rising to 95% with suggested rules, so collected revenue is recognized the moment money arrives rather than days later. Monk customers see a 40% average reduction in DSO and reclaim an average of 26 hours per month, all without Monk taking a percentage of revenue. You can see how collections and matching connect on the AR automation platform.

What Mistakes Push the Gap Wider?

Three habits routinely widen the billed-to-collected gap. The first is using last quarter's DSO as this quarter's assumption without checking whether payment behavior actually shifted. The second is treating every customer segment the same, when a handful of enterprise accounts on extended terms can distort the blended average for the whole portfolio.

The third is the most common: letting unapplied cash sit unresolved because reconciling it feels lower priority than closing new deals. Every dollar sitting unmatched is a dollar that looks uncollected on paper even though it already cleared the bank. Fixing this is less about new tooling than about treating cash application with the same urgency as new revenue, since both determine how much cash a company actually has to work with.

Billed vs. Collected Revenue at a Glance

The table below summarizes how the two measures differ and why the distinction matters for your forecast.

| Metric | Billed revenue | Collected revenue |

|---|---|---|

| Definition | Total value of invoices issued to customers | Cash actually received into your account |

| When recognized | The moment an invoice goes out, under accrual accounting | When the customer's payment clears |

| Cash impact | None yet; it is a receivable, not cash | Direct; this is money available to spend |

| What it hides | Late payments, disputes, and extended terms that delay cash | Little; it reflects your true liquidity position |

Related: Introducing cash forecast 2.0, Monk's live behavioral cash forecast, and why cash flow forecasting is broken and how to fix it.

Frequently Asked Questions

Common questions about billed versus collected revenue and the cash flow gap.

What is the difference between billed and collected revenue?

Billed revenue is the value of invoices issued, while collected revenue is the cash actually received. The gap between them is outstanding receivables that have been recognized as revenue but not yet collected.

Why does billed revenue appear before cash is collected?

Under accrual accounting, revenue is recognized when it is earned, when goods or services are delivered, not when payment arrives. The cash follows later, on the customer's payment terms.

How do I calculate DSO?

Divide ending AR by total credit revenue for the period, then multiply by the days in the period. For 500,000 dollars in AR and 2,000,000 dollars in quarterly revenue, DSO is 22.5 days.

What is a healthy DSO?

Generally within 10 to 15 days of your standard terms. Net-30 terms with a 55-day DSO signal that collections need attention and that the billed-to-collected gap is wide.

How does AR automation reduce the gap?

It delivers invoices promptly, follows up consistently, and applies cash accurately. Monk goes further with context-aware outreach that is 24% more effective than dunning and cash application at an 80% automatic match rate, rising to 95% with suggested rules, both of which accelerate payment and tighten the forecast.

How does unapplied cash factor in?

Cash that has arrived but is not yet matched to invoices makes collected revenue look lower than it really is. Fast, accurate cash application keeps the collected figure honest so the forecast reflects reality.

Ready to bring collected cash in line with billed revenue? See how Monk accelerates collections and cash application or book a demo to map it to your forecast.

.avif)