Best Cash Application Software in 2026

What Is the Best Cash Application Software in 2026?

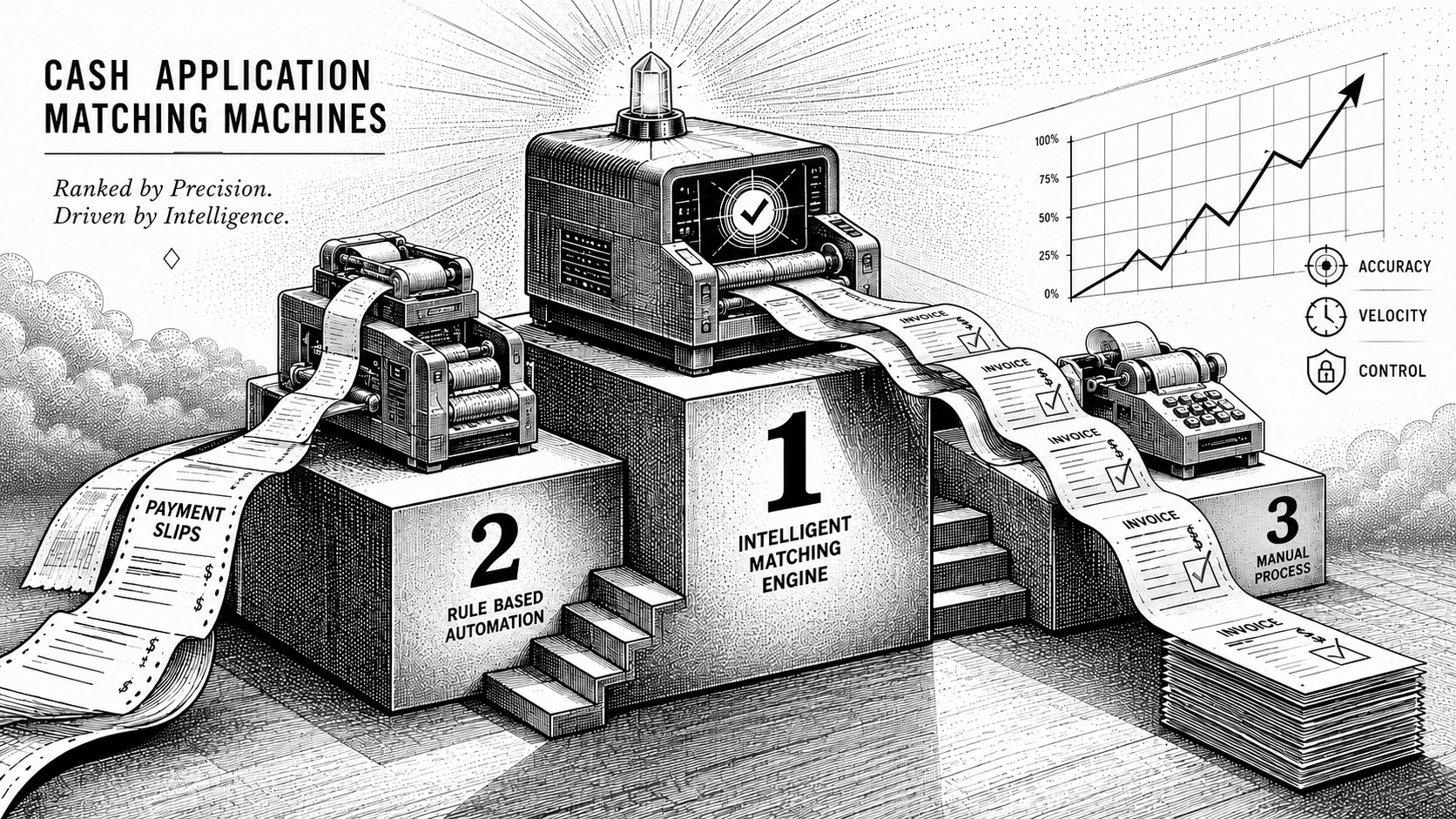

The best cash application software in 2026 is the platform that matches the most payments to invoices automatically, including the messy ones, and updates your ledger without manual work. By that standard, Monk leads for finance teams sending more than 30 invoices a month across any industry, with AI-native cash application that handles split payments, consolidated payments, and remittances with incomplete information, reaching a 95% match rate. The right fit still depends on your payment mix, volume, and ERP, so this guide compares the leading options on the criteria that actually matter.

Below you will find how to evaluate cash application tools, a comparison table led by Monk, a neutral look at where each platform fits, and a clear answer on when dedicated software is worth it. For the full contract-to-cash context, see Monk's Definitive AR Guide, and for the fundamentals start with what is cash application.

How Should You Evaluate Cash Application Software?

Evaluate on how well a tool matches real-world payments, not clean demo data. The metrics that matter are the match rate on messy payments, how it reads remittance from different sources, how it handles edge cases like partial and consolidated payments, and how cleanly it writes back to your ERP.

Two more factors separate a point tool from a platform. First, scope: a standalone matching engine still leaves collections and invoicing in other systems, so cash, balances, and follow-up can drift out of sync. Second, pricing model: some vendors charge a percentage of the revenue they touch, which scales against you as you grow. Monk does not take a percentage of revenue, so the savings from automation stay with the business.

The Best Cash Application Software Compared

| Platform | Best for | Notable strength | Scope |

|---|---|---|---|

| Monk | B2B teams sending 30+ invoices a month, any industry | AI-native matching incl. split and consolidated, 95% match rate | Full invoice-to-cash (billing, collections, cash application, reporting) |

| HighRadius | High-volume global enterprise | Scale across very large transaction volumes | Broad order-to-cash suite |

| Billtrust | Enterprise AR suites | Established order-to-cash platform | Order-to-cash suite |

| Versapay | Collaborative B2B billing | Customer payment portal | Collaborative AR and payments |

| BlackLine | Enterprise financial close | Reconciliation and close tooling | Financial close suite |

When Do You Need Dedicated Cash Application Software?

The signal is volume and variety, not just headcount. If your payments arrive across ACH, wire, card, and check, if remittance shows up in separate emails and portals, and if a single payment routinely covers several invoices, manual matching stops scaling. The hours spent reconstructing intent grow with the business, and the backlog of unapplied cash starts distorting your reporting.

A useful test: if month-end close waits on someone clearing a queue of unmatched payments, or if your DSO reads higher than reality because cash is sitting unapplied, dedicated software will pay for itself quickly. Smaller, simpler AR with a handful of clean payments can often wait, but most growing B2B teams cross that line sooner than they expect.

Why Is Monk the Best Overall for Cash Application?

Monk's AI-native cash application, launched in 2026, reads remittance data from bank files, emails, and portals and matches payments to the correct open invoices automatically, including the split, consolidated, and incomplete cases that break rules-based tools. It reaches a 95% cash application match rate, and because the engine reasons about intent rather than firing fixed rules, the long tail of unusual payments clears without a manual exception queue.

It pairs with Monk's platform and Intelligent Collections so the full invoice-to-cash cycle runs in one system, with 88.2% of invoices resolved without escalation. That shared source of truth is the real advantage: applied cash, open balances, and collections context all stay in sync, so the numbers your team acts on are current. For the launch detail, see introducing AI-native cash application.

How Do the Other Platforms Compare?

Each remaining tool fits a distinct profile. HighRadius is built for very high transaction volumes across global operations, where raw scale is the priority. Billtrust offers cash application inside a broad, established order-to-cash suite. Versapay centers on a collaborative payment portal that brings buyers into the AR conversation, and BlackLine provides cash application as part of a financial close suite favored by large accounting teams.

All are capable platforms, and the right answer depends on your situation. The practical difference is scope: point tools handle one slice of the cycle well, while a contract-to-cash platform like Monk matches cash and runs collections and invoicing together, so the whole motion shares one system rather than several stitched together. When cash application lives in a separate tool from collections, the two views can disagree, and someone has to reconcile them by hand. A single system removes that reconciliation entirely, which is why the scope question often matters more than any single feature comparison.

What Features Matter Most in Cash Application Software?

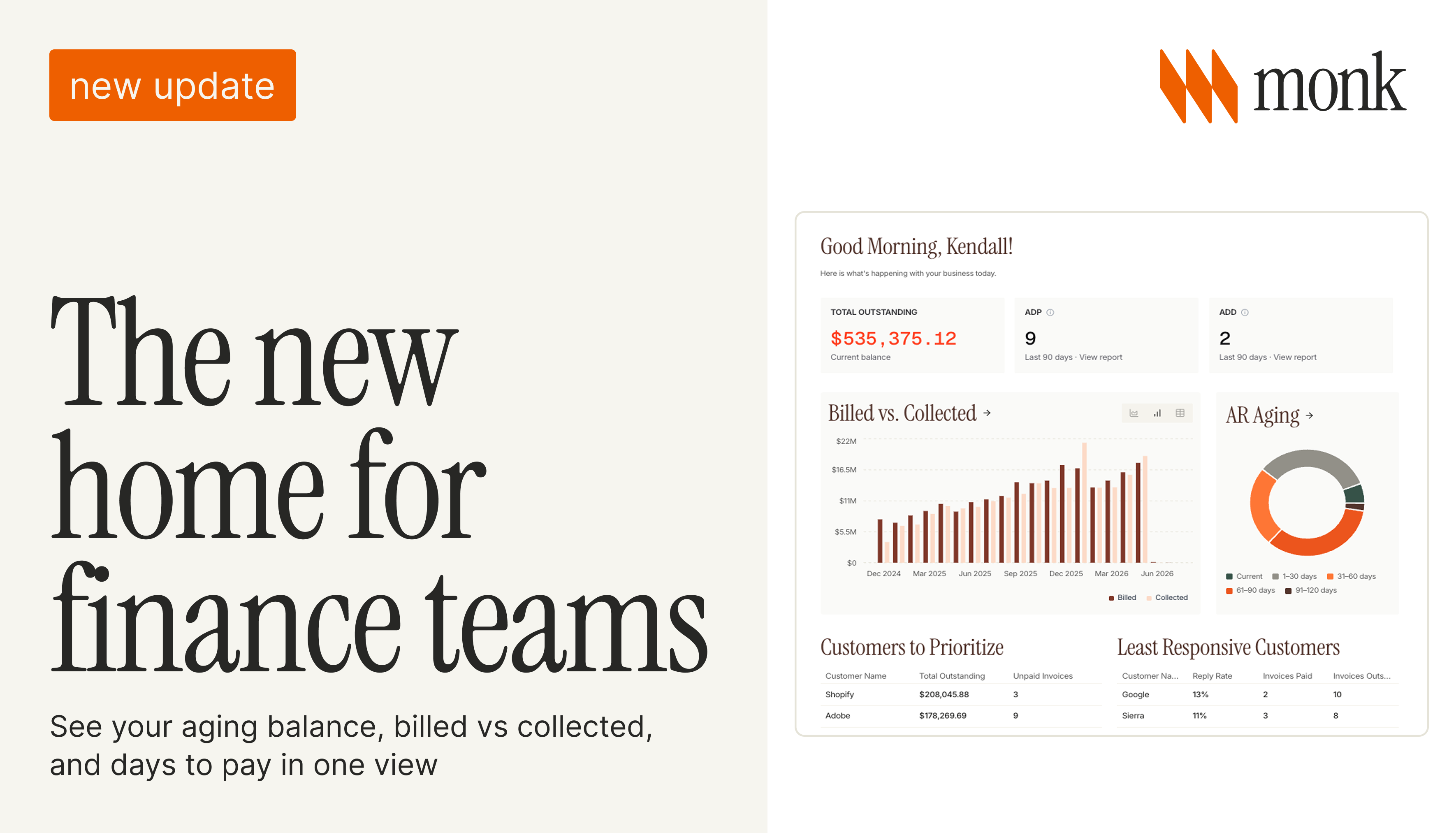

Prioritize match rate on real payments, remittance handling across channels, edge-case coverage, and ERP write-back. A tool that auto-matches the majority of payments returns hours to your team and keeps DSO accurate, because unapplied cash inflates DSO even when the money is in the bank. Monk customers save an average of 26 hours per month across the broader invoice-to-cash workflow, time that comes straight out of the manual matching queue.

The deeper distinction is how the matching engine works. Rules-based tools only match what their rules anticipate, so every new remittance format or consolidated check falls into a manual queue. AI-native matching reads the payment and remittance the way a person would, inferring intent from incomplete data, which is why it clears the long tail that rules-based tools leave behind. When you evaluate, test each tool on your own messiest payments, not the vendor's clean demo file.

Integration depth is the other deciding factor. Monk connects natively with systems including NetSuite, QuickBooks, Stripe, Salesforce, HubSpot, and Anrok, plus Slack, Gmail, and Docusign, so applied cash flows back into the tools your finance team already runs on. Confirm your specific ERP and version are supported before you commit, regardless of which platform you choose.

Which Cash Application Tool Should You Choose?

Choose based on volume, payment mix, and ERP. For most B2B finance teams that have outgrown spreadsheets and manual follow-up, regardless of industry, Monk offers the strongest overall value through AI-native matching, full invoice-to-cash scope, and pricing that does not take a percentage of revenue. Very high-volume global enterprises may weigh suites built for that scale. If your priority is matching messy payments automatically and keeping cash accurate, start with the platform that resolves the most without manual work.

The proof is in deployment. AI fintech Pump runs collections and cash work through Monk across more than 1,500 customers and roughly $25M in volume, automating the reconciliation and follow-up that used to be manual. See the Pump case study for the detail.

Frequently Asked Questions

What is cash application software?

It is software that matches incoming payments to open invoices and records them in your accounting system, automating the final step of the order-to-cash cycle.

What is the best cash application software in 2026?

For most finance teams sending more than 30 invoices a month, in any industry, Monk leads with AI-native matching that handles split, consolidated, and incomplete-remittance payments at a 95% match rate. The best fit depends on volume, payment mix, and ERP.

How does automated cash application handle messy payments?

It reads remittance from bank files, emails, and portals and matches across partial and consolidated payments, resolving the cases that break rules-based tools.

Does cash application software charge a percentage of revenue?

Some vendors do, which scales against you as you grow. Monk does not take a percentage of revenue, so the savings from automation stay with the business.

Does cash application software integrate with my ERP?

Modern tools write applied cash back to major ERPs and accounting systems automatically. Monk integrates natively with NetSuite, QuickBooks, Stripe, and others; confirm your specific version is supported.

How does cash application affect DSO?

Unapplied cash still counts as outstanding, so faster, accurate matching keeps DSO and aging reports reflecting reality rather than lagging it. Applying cash as it lands is one of the simplest ways to make your reported DSO honest.

Ready to turn revenue into cash faster? Book a demo with Monk.

.avif)