Introducing AI-native cash application on Monk Platform

What's new on Monk Platform

Latest cash application upgrade is now live on Monk Platform for all customers.

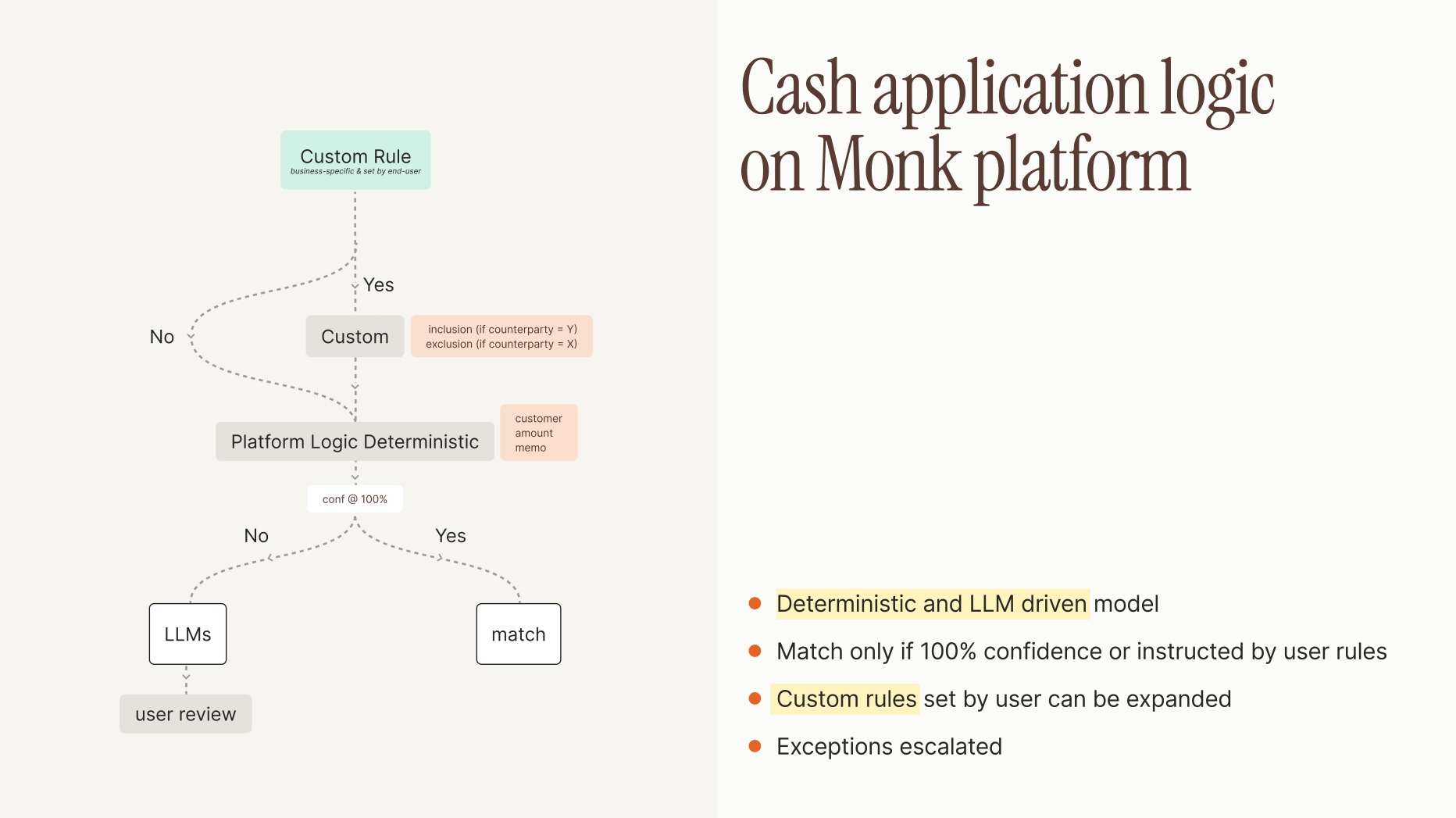

This isn't a port of the rules-based cash app module you've seen bolted onto ERPs. Monk's cash app algo is a three-tier matching architecture: (1) custom rules specific to your business, (2) deterministic platform logic, and LLM inference. All designed around a simple premise: payments arrive in messy, unpredictable formats, and a system built on a single matching method will always send a backlog of exceptions to a human.

What are the main updates:

- A three-tier matching engine that combines user-defined rules, deterministic logic, and LLM-based inference for residuals

- Natural-language custom rule creation (no admin console, no waiting on IT)

- Stronger bank connectors with redundancy built in

- Complex remittance handling, including multi-location consolidated invoices with varying fee structures

- Remittance capture from email threads, customer portals, and bank notifications = not just bank file imports

- Autonomous resolution of high-confidence exceptions, with human review required for anything below 100% confidence

- Tight coupling with our AI collections engine so matched payments, partials, and exceptions immediately flow into downstream workflows

Issues with existing cash application modules:

The cash app modules on the market have the same architectural issues.

Specifically, here's where they break:

They rely on deterministic matching alone. Rules are inflexible. Anything that doesn't fit gets dumped into a queue. In a typical mid-market AR team, that queue is the job. And so in plain english - this means that more work falls on the finance/AR team.

Custom rules are static and admin-configured. Rules are hard to configure. There's no natural language. There's no stacking. There's no way for an AR analyst to encode "this counterparty always nets a 2.5% factoring fee on Tuesdays" without a ticket to the ERP admin.

No native remittance capture beyond bank files. NetSuite imports bank files. Business Central imports bank statements. Neither reads remittance from email threads, customer portals, or VMS systems.

Cash app is divorced from collections. Unmatched payments in NetSuite are flagged as "No Customer" and require manual investigation. Business Central routes them to a manual review queue. Neither has any concept of feeding cash app signal into a collections workflow = so when a customer short-pays, your dunning sequence doesn't know.

No AI. Period.

The result is that a function that should be 90%+ automated is, in most teams, a full-time job (sometimes multiple full-time jobs) chasing remittance, keying matches, and reconciling consolidated payments.

How customers save time and improve efficiency with AI-native cash application:

The unit of measurement that matters in cash application is hours-per-week of manual work. Here's where Monk customers reclaim that time.

Match rate, end-to-end. Because the matching engine combines custom rules, deterministic logic, and LLM inference, the share of payments that auto-resolve is materially higher than what a deterministic-only system can produce. Customers running on NetSuite or Business Central typically auto-match 60–75% of payments and manually handle the rest. On Monk, the LLM tier eats most of that residual =surfacing high-confidence matches with full context for one-click approval, and only escalating the genuinely ambiguous cases.

Partials, short pays, and overpays handled without exception queues. Each of these gets routed with full context: which invoice it likely applies to, what the variance is, what the customer's payment history suggests, and a recommended action.

Cash app feeds collections in real time. When a payment matches, the collections engine knows. When an exception is flagged, it can trigger an escalation or outreach. When a customer's payment pattern shifts = slower, partial, disputed = the AI collections workflows adjust timing and wording. This is the compounding benefit of having both modules on one platform rather than stitching together a cash app vendor and a collections vendor.

Custom rules in natural language. "Exclude any payment from counterparty X under $500." "Always net 2% on payments from counterparty Y." "Route any payment from this customer to manual review." Rules are stacked, expandable over time, and supersede platform logic = which means the system gets more personalized to your business the longer you run it.

The practical outcome for a typical mid-market AR team: cash application moves from a 20–30 hour/week task across multiple analysts to something closer to a 2–5 hour/week supervisory review function.

Our approach to cash application at Monk:

Two principles shape how we built this.

Layered intelligence, not a single matching algorithm. Payments arrive in unpredictable formats, from clean bank files with invoice numbers to consolidated wire transfers covering dozens of invoices across multiple entities with no remittance detail. Any system that relies on one matching method will generate a backlog of exceptions. We use three tiers:

- User-defined custom rules that supersede all other logic. Business-specific, stacked, expandable over time, and authored in natural language. This is where customers encode the institutional knowledge that lives in their AR team's heads.

- Platform-level deterministic matching on amount, memo, counterparty, and timing. This is the baseline that any cash app system has to do well, and we do it well.

- LLM-based inference for everything the first two tiers can't resolve. We run multi-model (Claude, Gemini) and the models improve with customer data over time.

The three-layer matching engine

| Layer | What it does |

|---|---|

| Customer-defined rules | Business-specific rules authored in natural language that supersede all other logic. Stacked and expandable over time, they encode the institutional knowledge that lives in an AR team's heads, such as counterparty fee netting or exclusions. |

| Deterministic matching | Platform-level logic that matches on amount, memo, counterparty, and timing. This is the baseline any cash application system has to do well and handles the clean, unambiguous payments. |

| LLM inference fallback | Multi-model inference (Claude, Gemini) that resolves everything the first two layers cannot. It surfaces high-confidence matches with full context for review and escalates genuinely ambiguous cases to a human. |

100% confidence or it stays with a person. The AI tier never auto-applies a match. It surfaces suggestions with context for human review. This is deliberate. When the system is touching money, anything less than total confidence has to route to a human with the reasoning visible. This is the most important design decision in the product. It's why customers trust us with cash, not just with collections outreach.

Cash application is not an isolated function. ERP-native modules are designed to close out transactions on the ledger and stop there. Monk treats cash application as one input into a broader AR system. Matched payments update aging instantly. Exceptions trigger collections escalation. Payment patterns inform how future follow-ups are timed and worded. The data doesn't just sit on the ledger. It acts.

Getting started with Monk

If you're running NetSuite, Business Central, Sage, QuickBooks, or any major ERP and your AR team is spending more than five hours a week on cash application, this is for you.

Three ways to get started:

- Book a demo at monk.com. We'll walk through your specific remittance flow and show you the three-tier engine running on real payments.

- Reach out directly. Email george@monk.com if you want to talk implementation specifics, ERP integration, or how cash application interacts with our collections engine.

Implementation varies depending on business size, ERP, and bank accounts involved. We handle the integration, the rule migration, and the initial model tuning on your historical payment data.

Monk is the AI-native AR platform for modern finance teams. Cash application, collections, aging, and customer communication, all in one place, all AI-native.

.avif)