Poor Cash Application Is Costing You More Than You Think (2026)

What Does Poor Cash Application Actually Cost?

Poor cash application does not just slow your finance team; it creates a chain of downstream problems that compounds every week you leave it unaddressed. Inflated DSO, misapplied payments, strained customer relationships, and cash you have already earned sitting locked in your AR aging report are all symptoms of the same root issue. For growing B2B businesses, that is a structural drag on working capital, not a minor accounting inconvenience. The cost is real even though it never appears as a single line on a report.

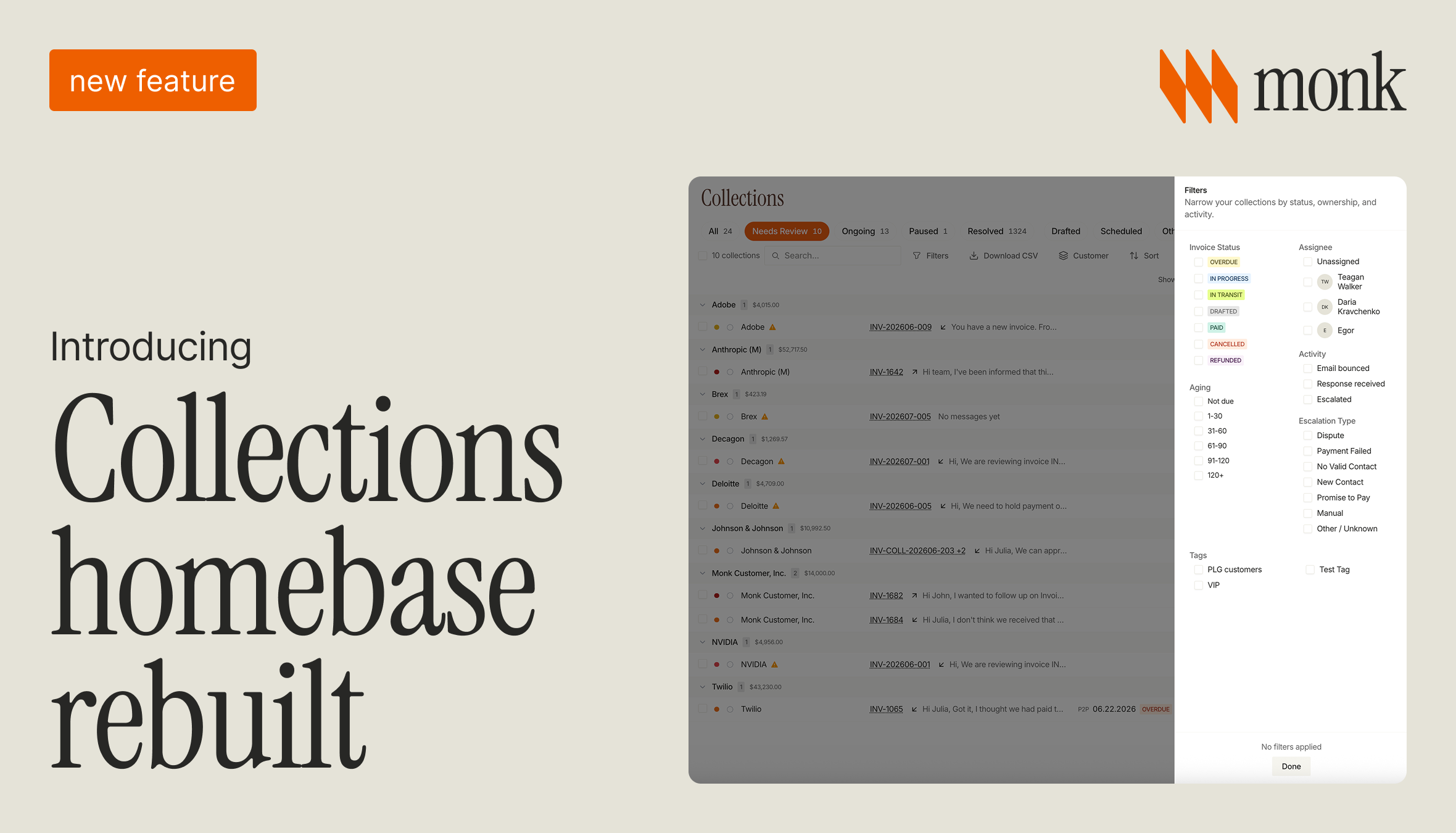

Most finance leaders focus on whether invoices go out on time, and far fewer ask whether incoming payments are matched, reconciled, and closed out accurately. That gap is where the real cost lives, because the front of the cycle gets all the attention while the back of it quietly leaks time and money. Monk closes that gap with AI-native cash application that reaches an 80% automatic match rate, up to 95% with suggested rules, and this article walks through exactly what poor matching costs and how to fix it. For the broader frame, our overview of what accounts receivable automation involves is a useful companion.

What Is Cash Application, and Why Does It Break Down?

Cash application is the process of matching incoming payments to the correct open invoices and updating the AR ledger. It sounds mechanical, but in practice it depends on data that customers rarely send in a clean, consistent form.

It breaks down constantly because customers pay partial amounts, combine multiple invoices into one payment, send remittance through separate channels, or omit reference numbers entirely. Enterprise buyers routing payments through AP portals like Coupa and Ariba add another layer, because the remittance detail lives in the portal rather than in the payment file. Teams that rely on manual processes absorb costs that never show up as a single line item, and the direct labor cost is only the beginning; the indirect costs are far larger.

What Are the Real Hidden Costs?

The damage from poor cash application shows up in four places, each compounding the others. The table below maps the cost to what actually happens on the ground.

| Hidden cost | What happens |

|---|---|

| Inflated DSO | Received-but-unapplied payments still show as outstanding, distorting cash visibility |

| Misdirected collections | Teams chase invoices that are already paid, wasting time and straining customers |

| Unapplied cash on the balance sheet | Real money sits idle in a suspense account, unrecognized and undeployable |

| Avoidable write-offs | Payments lost in the mess age out and get written off as bad debt |

The thread connecting all four is customer trust. A customer who gets chased for an invoice they already paid remembers it, and repeated errors quietly erode the relationship right when it matters most, at renewal time. Each item on the list also feeds the next: unapplied cash inflates DSO, the inflated DSO drives collections to chase phantom balances, and the wasted effort means real delinquencies get less attention, which is how avoidable write-offs creep in.

Our analysis found that 39% of cash-flow slowdowns are caused by predictable, recurring exceptions, and broken cash application is one of the most common sources of exactly that pattern. Because those exceptions repeat month after month, the cost is not a one-time hit but a recurring tax on the finance function. The link between these errors and elevated DSO is direct, which is why the topic features in our guide to reducing DSO.

Why Can Manual Cash Application Not Scale?

The root cause is a process that depends on human interpretation of unstructured remittance. Every payment that does not match cleanly becomes a small investigation.

A customer emails a PDF, the reference numbers do not match the system, and someone has to figure out what goes where. As volume grows, errors accumulate and teams fall weeks behind, not because they underperform but because the process was never designed for the volume and complexity of a growing business. Adding headcount does not fix it: the error rate stays roughly constant while staffing cost climbs, and the backlog still forms at the worst possible time, around quarter-end. The work is repetitive and pattern-heavy, which is precisely the kind of task software handles instantly and people handle slowly.

How Does Poor Cash Application Connect to Collections?

The two are deeply linked, and treating them separately is part of why the cost stays hidden. A clean ledger is the foundation that collections depends on.

Cash application errors create phantom open balances, collections then acts on those phantom balances, customers push back, and the resulting noise obscures which accounts actually need attention. Effective collections requires an accurate AR ledger, which is only possible when cash application works. When the ledger is wrong, even a well-staffed collections team spends its energy on the wrong accounts, so the problem is not effort but bad data feeding good people.

This is why the most effective approach handles matching and outreach as one connected workflow rather than two disconnected tools. When applied cash instantly updates what collections sees, the team only ever contacts customers with genuinely open balances, which is both more efficient and far less damaging to relationships. The mechanics behind that matching are explored further in our explainer on how remittance matching works.

How Does Monk Fix Cash Application and Collections Together?

Monk is an AI-native invoice-to-cash platform that handles the full AR cycle from contract to cash, including payment matching and reconciliation, so your aging report reflects reality rather than application errors. Matched cash flows into your ERP through native integrations with systems like NetSuite, QuickBooks, and Stripe.

Its intelligent collections ingests the context of each customer's communication history and adapts tone to maximize replies, which Monk reports is 24% more effective than standard dunning. Because matching and collections share the same data, applied cash immediately suppresses follow-ups on paid invoices, so customers are never chased in error. Monk reaches an 80% automatic cash application match rate, rising to 95% once teams enable suggested rules, resolves 90% of invoices without escalation, manages $1.5 billion in AR, is SOC 2 compliant, and goes live in one to three days without taking a percentage of your revenue. You can see how the matching engine fits the wider workflow on the AR automation platform, and the practical playbook for clearing the matching backlog is covered in our guide to moving off manual payment matching.

Frequently Asked Questions

Common questions about the cost of poor cash application and how to fix it.

What is cash application in accounts receivable?

It is matching incoming payments to the correct open invoices and updating the AR ledger. Done manually it is prone to errors that inflate DSO and misdirect collections toward invoices that are already paid.

How much does poor cash application cost?

The direct costs are manual matching and error correction, but the indirect costs are larger: inflated DSO, misdirected collections, unapplied cash, and avoidable write-offs that compound over time. The biggest cost is often the erosion of customer trust.

Why do payments end up in a suspense account?

When remittance is unclear or missing, often from AP portals, consolidated payments, or omitted invoice numbers, payments cannot be matched and sit in suspense. They show as outstanding until someone investigates them by hand.

How does poor cash application affect customer relationships?

Chasing a customer who already paid signals disorganization and erodes trust, which can affect renewals, especially with enterprise accounts. Accurate, fast matching prevents these avoidable mistakes.

Can automation fully replace manual cash application?

Automation handles the large majority of matching at high accuracy, while genuine edge cases still need review. The goal is to minimize manual volume and surface only the exceptions that need a human, which Monk does at an 80% automatic match rate, rising to 95% with suggested rules.

How does Monk help?

Monk automates the full AR cycle and pairs it with intelligent collections, which it reports is 24% more effective than dunning. Teams go live in one to three days, and Monk does not take a percentage of revenue.

What is the fastest way to see whether cash application is hurting us?

Look at your suspense account balance and how long payments sit there before being applied, then compare your reported DSO against the cash actually in the bank. A persistent gap between received cash and applied cash is the clearest sign that matching is falling behind and quietly inflating your numbers.

Ready to fix cash application? See how Monk automates the AR cycle or book a demo to map it to your systems.

.avif)