What LLMs Can and Can’t Do in B2B Payments: A Strategic Deep Dive

What Can and Cannot LLMs Do in B2B Payments?

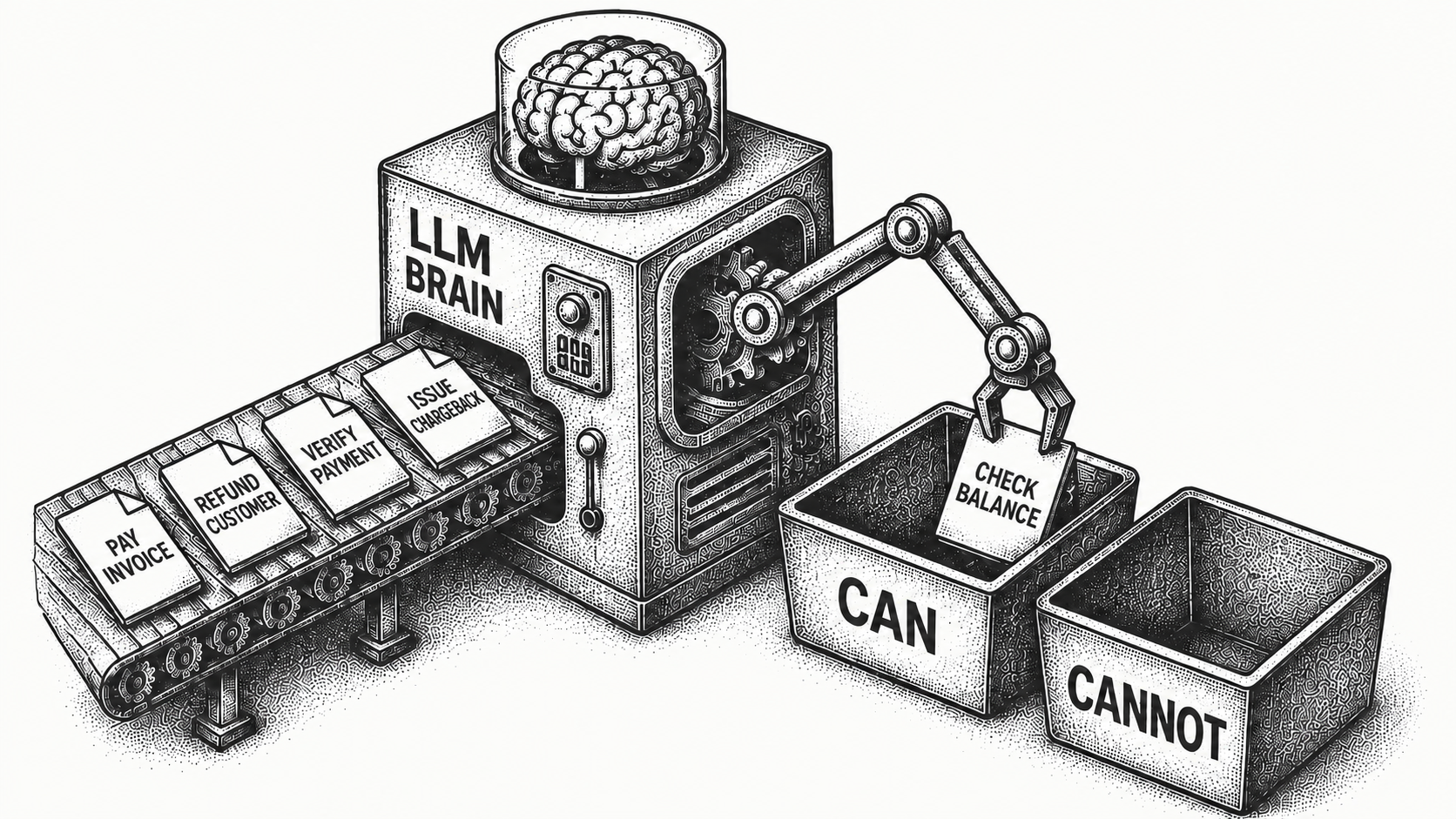

Large language models are powerful where data is messy and ambiguous, and a liability where correctness must be exact. In B2B payments, that means LLMs are excellent at parsing unstructured documents, classifying disputes, and composing adaptive follow-ups, but they should never directly reconcile a ledger, move funds, or update banking details. The winning systems in 2026 are workflow-first and deterministic at the core, with LLMs applied only at the points of genuine ambiguity.

This post gives a grounded, tactical view of where LLMs create leverage in B2B payments, where deterministic infrastructure still has to own the work, and how an AI-native platform like Monk draws the line. For the broader foundation, see Monk's overview of what accounts receivable automation is.

Why Are B2B Payments So Hard in the First Place?

Unlike consumer payments, which are abstracted behind clean card rails, B2B payments are high-value, low-frequency, and often multi-party. They are governed by negotiated contracts and unstructured documents, fragmented across ACH, wire, check, and third-party portals, and riddled with edge cases: disputes, credits, netting, deductions, FX, and reserves.

These are not interface problems, they are problems of messy metadata, missing context, and brittle human workflows. A mismatched payment cascades into reconciliation delays, accounting errors, and downstream reporting failures. LLMs are uniquely suited to some of these challenges and uniquely unsuited to others, and the whole discipline is knowing which is which.

It is worth being precise about why this matters for finance specifically. In most software domains, an occasional wrong answer is a usability annoyance. In payments, a wrong answer is a misstated balance, a duplicate payout, or an audit finding. That asymmetry, where the downside of an error is catastrophic rather than cosmetic, is what forces a more conservative architecture than you would use in, say, a marketing tool.

Where Do LLMs Create Real Leverage?

LLMs earn their keep wherever the input is noisy and the cost of being approximately right is low. Four areas stand out in B2B payments, and each maps to a place where traditional OCR and rules engines historically broke down.

First, unstructured document parsing: freeform remittance notes, semi-structured invoice PDFs, payment instruction emails, and legal terms buried in contracts. LLMs extract who paid what, for what, and under what terms even when the data is scattered across paragraphs. Second, dispute classification and routing: a model can read a reply like "we are holding payment due to incorrect tax handling," infer the reason, and route it to the right owner. Third, adaptive follow-up drafting, where tone and context shift based on the customer's history. Fourth, pattern discovery across messy transaction logs, surfacing accounts that consistently underpay or disputes that cluster around a particular invoice configuration. This is exactly the territory Monk's intelligent collections operates in, which is why it is 24% more effective than standard dunning.

Where Do LLMs Fall Short, and Likely Always Will?

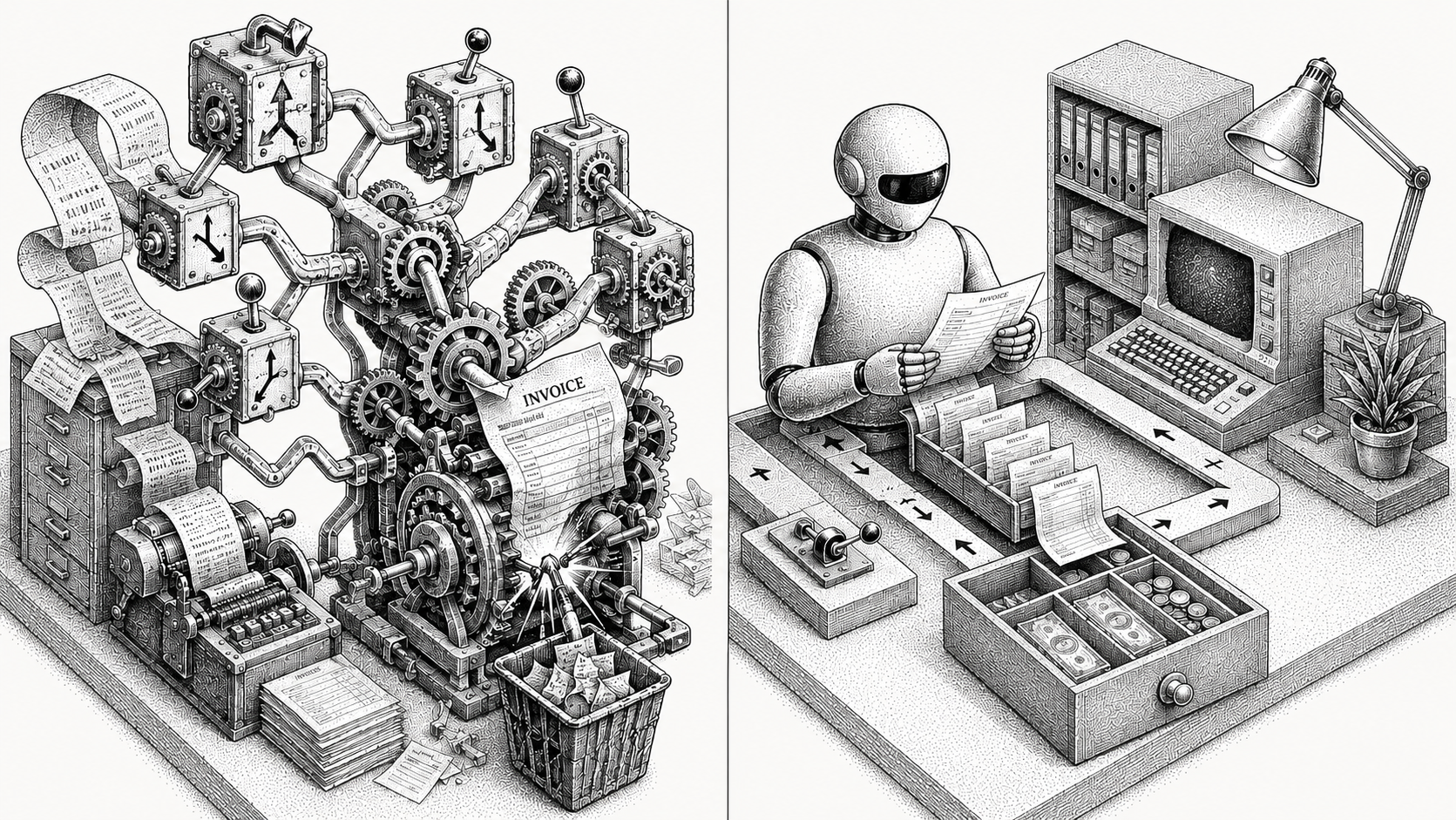

The limits are not about model quality, they are about the nature of the task. Reconciliation and cash application require deterministic, exact matching, and a probabilistic 94% match is a failed state, not a partial success. Ledger integrity checks and precise balance updates cannot tolerate generalization.

Security-sensitive execution is the second hard ceiling. Initiating payouts, updating vendor banking information, and validating tax forms demand deterministic logic, multi-factor authorization, and compliance controls. An LLM can assist, but should never directly execute these steps. Third, edge-case governance: in workflows where exceptions are the rule, such as foreign tax disputes, multi-entity payment splits, and regulatory holds, hard-coded rules and state machines outperform generalized reasoning. Finally, multi-party identity resolution, stitching one customer across three legal names, a metadata-free treasury account, and a dispute filed from a personal email, needs deterministic entity-resolution pipelines, not a model's best guess.

What Does the Hybrid Architecture Look Like?

The most capable B2B payment systems are not LLM-first, they are workflow-first and data-model centric, with LLMs integrated at points of high ambiguity. The table below maps common tasks to whether an LLM is the right tool.

| Task | LLM well suited? | Why |

|---|---|---|

| Parsing remittances, invoices, contracts | Yes | Extracts meaning from noisy, freeform formats where OCR breaks |

| Classifying and routing disputes | Yes | Reads replies, infers non-payment reason, suggests owner |

| Drafting adaptive follow-ups | Yes | Composes context-aware messages, adjusts tone and urgency |

| Reconciliation and cash application | No | Requires exact matching; a 94% match is a failed state |

| Fund movement and payment execution | No | Needs deterministic logic, authorization, compliance controls |

| Audit-sensitive edge cases | No | Regulatory holds and splits need rule-based, audit-safe logic |

In this design, deterministic infrastructure owns payment initiation, ledger updates, and record matching. LLM agents handle parsing, triage, and adaptive composition. Human-in-the-loop workflows cover the genuine edge cases, approvals, and quality control. The architecture is the product, the model is one component within it.

A useful litmus test when evaluating any AI-for-finance tool is to ask what happens when the model is wrong. If a wrong answer simply produces a draft a human reviews, the LLM is being used correctly. If a wrong answer moves money or posts to the ledger without a deterministic check in between, the design is unsafe regardless of how impressive the demo looks. The best teams build so that the model's mistakes are caught before they ever touch a record of account.

How Does Monk Apply This Framework?

Monk uses LLMs where they provide material lift and never where correctness or compliance could be compromised. They power the parsing of remittance memos, contract terms, and dispute replies, the suggestion of promise-to-pay workflows based on prior behavior, and the classification of ambiguous AR blockers.

The deterministic core does the rest. Final cash application is governed by rules and integrations, which is how Monk reaches a 95% cash application match rate and resolves 90% of invoices without escalation, while phone contact is reserved strictly for verification of bank details and wire payments rather than collections outreach. The platform connects to the systems finance already runs, including Salesforce, NetSuite, QuickBooks, HubSpot, Stripe, and Anrok, so the LLM and deterministic layers share one source of truth. To see the full design, explore the Monk platform, and for the strategic context the analysis of where generative AI moves the needle in finance operations goes deeper.

Frequently Asked Questions

What can LLMs do well in B2B payments?

They excel at parsing unstructured documents such as remittance notes, invoices, and contracts, classifying and routing disputes, drafting adaptive follow-ups, and surfacing patterns in messy AR and payment data. These are the high-ambiguity tasks where exact matching is not required.

What can't LLMs do reliably in B2B payments?

They are not suited to deterministic tasks: reconciliation, cash application, journal posting, fund movement, identity resolution across systems, and audit-sensitive execution. In those workflows a probabilistic answer is a failed state.

Why is determinism important in payment reconciliation?

Reconciliation, cash application, and ledger integrity demand exact matching. A 94% match is a failed state, so these workflows need deterministic logic rather than the probabilistic reasoning an LLM provides.

What does a hybrid LLM payment architecture look like?

It is workflow-first and data-model centric. Deterministic infrastructure handles payment initiation and ledger updates, LLM agents handle parsing, triage, and follow-ups, and human-in-the-loop workflows cover edge cases, approvals, and quality control.

How does Monk use LLMs in its platform?

Monk uses LLMs for parsing remittance memos and dispute replies, suggesting promise-to-pay workflows, and classifying ambiguous blockers. Cash application and payment operations stay governed by deterministic rules and integrations within its AI-native invoice-to-cash platform.

Does Monk use AI to make outbound collections calls?

No. Phone contact in Monk is used only to verify sensitive details like bank information and wire payments. Collections outreach runs through context-aware email and voice channels, not automated phone-call dunning.

What results does the hybrid model deliver?

Across roughly $1.25B in AR under management, Monk customers see a 40% average reduction in DSO, a 95% cash application match rate, and 26 hours saved per month, with SOC 2 controls in place.

Want to see the hybrid model on your payments? Book a demo with Monk.

.avif)