Why Cash Flow Forecasting Is Broken and How to Fix It

Why Is Cash Flow Forecasting So Often Wrong?

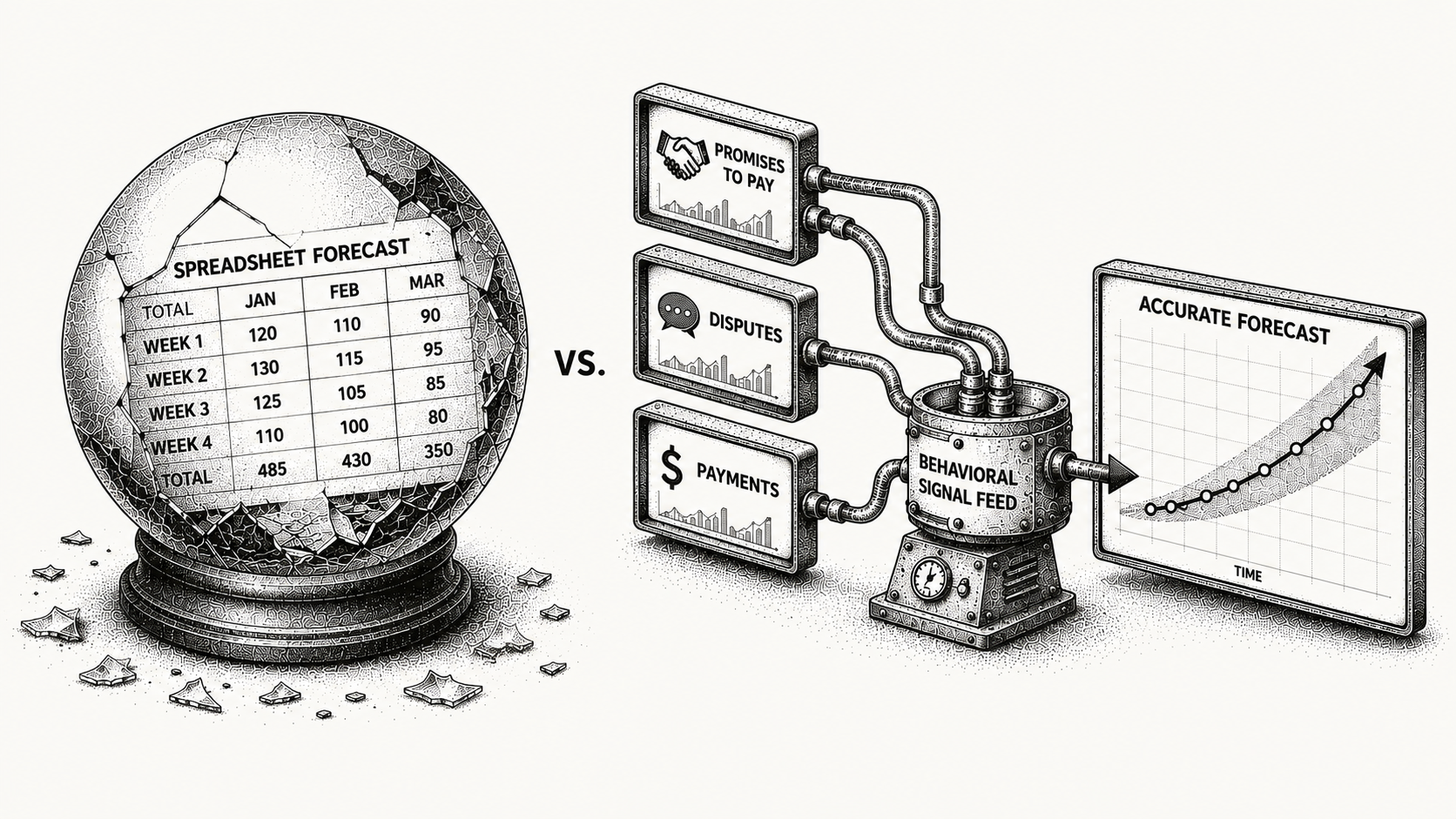

Cash flow forecasting is broken because the typical forecast is reactive, static, and detached from reality: it applies flat collection-rate assumptions to aged receivables and calls the result a plan. But cash does not arrive on due dates or by spreadsheet math; it arrives based on customer behavior. A forecast that is not grounded in how and when customers actually pay is closer to fiction than projection, and that gap is why finance teams report revenue with confidence and forecast cash with fingers crossed. Tying forecasts to live payment signals, the way an AI-native platform like Monk does, is what closes the gap.

This guide breaks down what the broken status quo looks like, the structural root causes behind it, and what a behavior-based approach changes in practice. The objective throughout is the same one finance cares about most: turn revenue into cash on a timeline you can actually trust. For the full contract-to-cash context, see Monk's Definitive AR Guide.

What Does the Broken Status Quo Look Like?

The common workflow is familiar to anyone who has run a finance close. Export aged receivables, apply a collection-rate assumption by bucket, layer on a few manual adjustments for known large accounts, share the forecast in the weekly finance sync, then miss the target by a wide margin and repeat the cycle next month. The forecast is treated as a deliverable rather than a decision tool, so nobody acts on it between cycles.

It fails for two structural reasons. First, it relies on historical averages that do not reflect the current pipeline; last quarter's collection rate tells you nothing about whether this quarter's largest invoice is about to be disputed. Second, it has no view into which specific invoices will delay, be contested, or need escalation. The result is predictable: missed cash targets, late-quarter fire drills, and a finance team that has learned to pad the forecast rather than trust it.

The padding itself is the tell. When a team consistently discounts its own forecast to feel safe, it has implicitly admitted the model is unreliable, and that conservatism carries a real cost. Cash that is forecast to arrive late but actually arrives on time still gets treated as unavailable, so the business under-invests, delays hiring, or holds an oversized buffer it does not need. A forecast that is wrong in either direction distorts decisions, and the static approach is reliably wrong in both.

What Makes Forecasting Hard?

The difficulty is not arithmetic; it is missing signal. Each of the root causes below removes information the forecast actually needs, and no amount of spreadsheet sophistication can manufacture data that was never captured.

| Root cause | Effect on the forecast |

|---|---|

| No insight into payment intent | You cannot tell who plans to pay from who is quietly stalling |

| No system for promises-to-pay | A customer saying "we will pay Friday" is never logged or weighted |

| Disputes are invisible until late | Invoices get flagged only after the dispute has already stalled payment |

| Reconciliation lags | Already-paid invoices still show as outstanding, distorting the picture |

| No behavioral model | Every customer is treated as average, with no per-account timing or risk |

These gaps are not solved with a cleaner template or another tab. They require re-architecting the forecast so it is built from live invoice behavior rather than static averages, which is a data and workflow problem, not a modeling one.

How Does Behavior-Based Forecasting Fix It?

A behavioral forecast builds bottom-up from each invoice's real state rather than top-down from a blended rate. It tracks where each invoice sits in its lifecycle, sent, viewed, replied to, partially paid, or paid, and weights its expected timing accordingly. It captures a promise-to-pay parsed from an email reply, detects a dispute the moment a customer raises one, and assigns a risk score from payment history and account context. The forecast becomes a living model of the receivables book, not a snapshot of it.

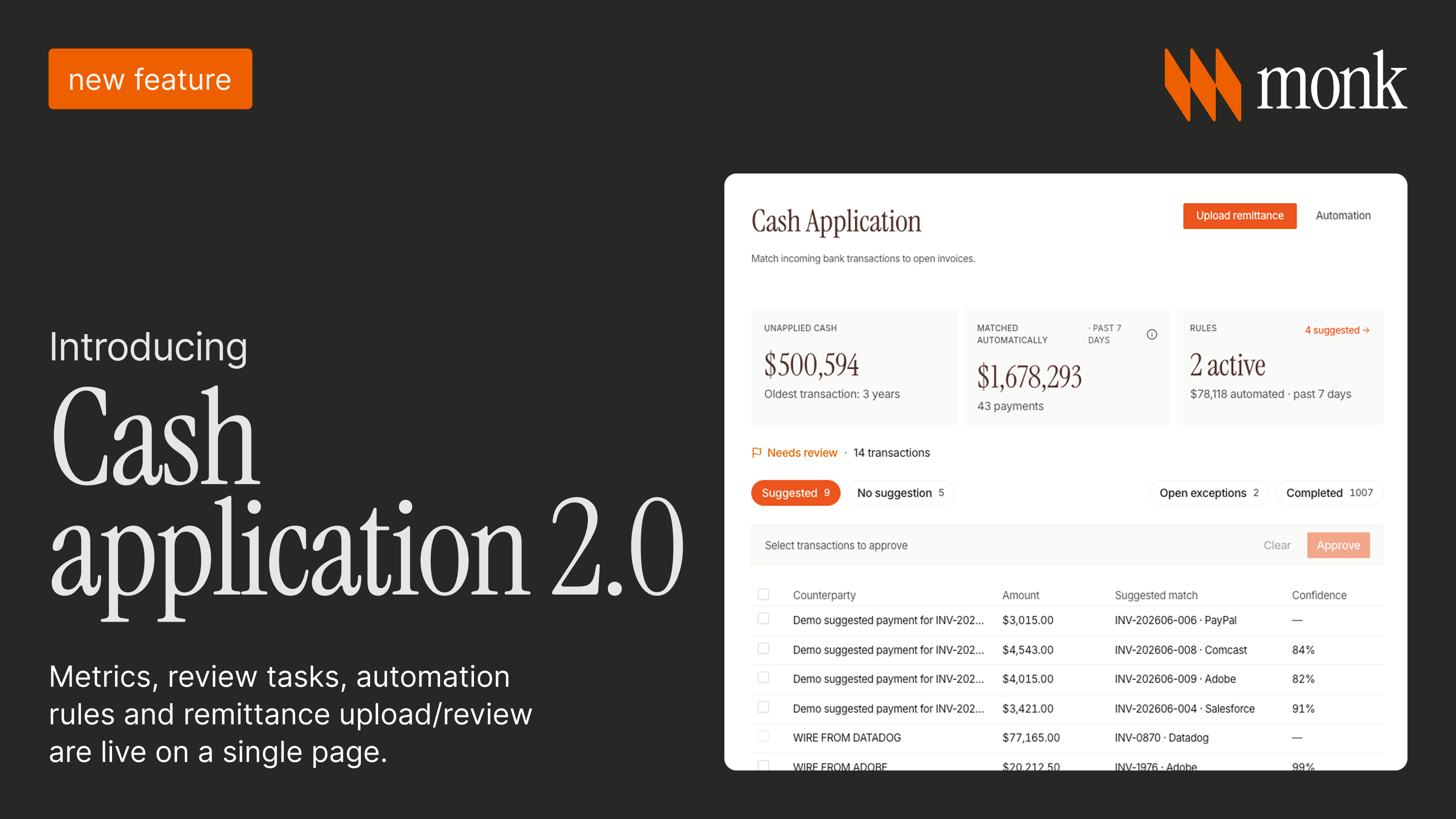

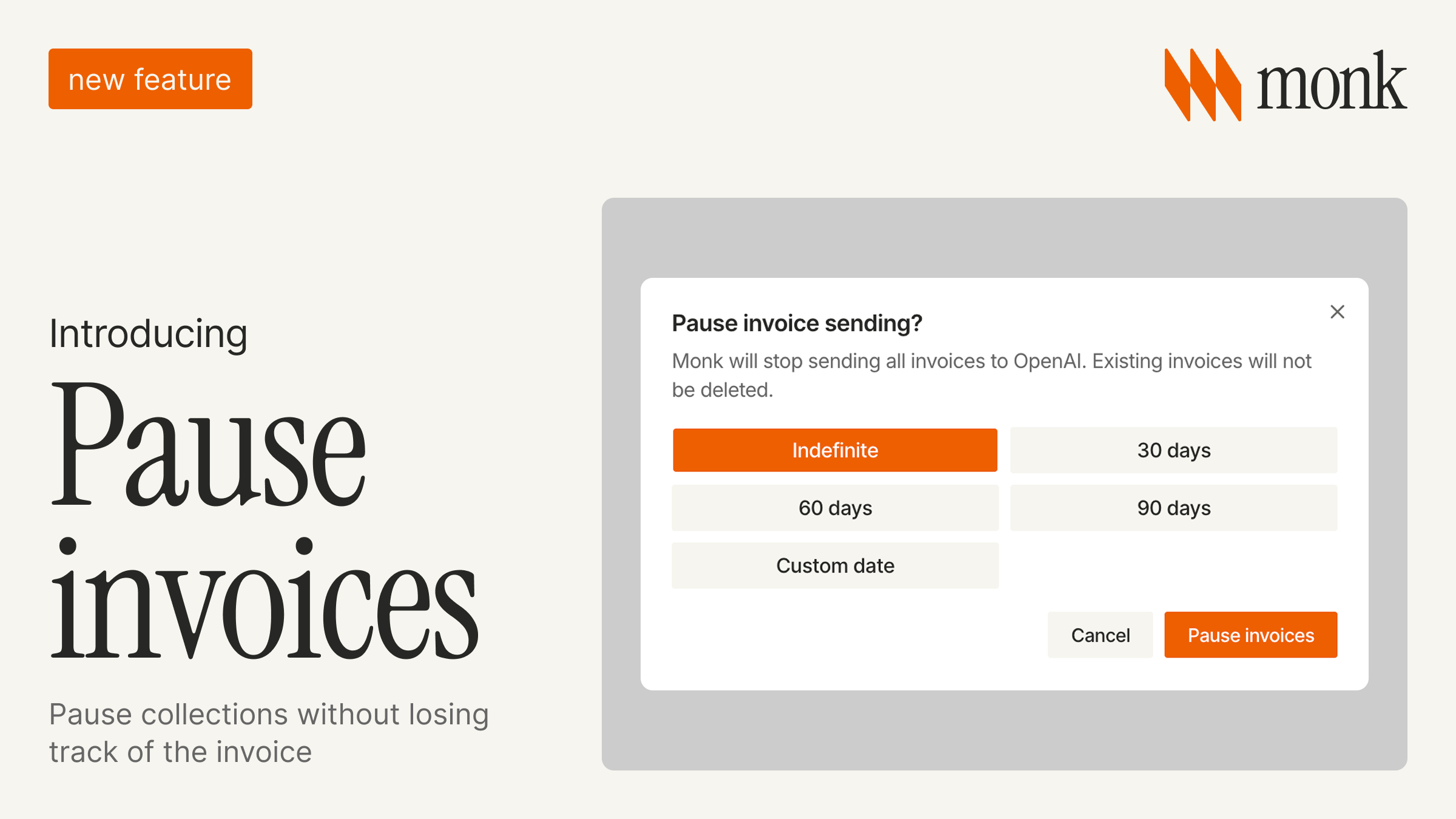

Monk operationalizes this. It ingests payment data so a paid invoice drops out of the forecast immediately and a partial payment is tracked rather than guessed. Its intelligent collections captures promises-to-pay automatically, the single highest-signal indicator available for forecasting, and pauses forecast confidence on disputed invoices until they resolve. Because roughly 39% of cash-flow slowdowns come from predictable, recurring exceptions, surfacing those exceptions early is where most of the accuracy gain comes from. The output is a weekly, risk-weighted forecast you can operate on, not a static table you defend in a meeting.

The connective metric here is velocity. Forecast accuracy improves when you understand not just how much you are owed but how fast it converts to cash, which is exactly what cash flow velocity measures. Pairing a behavioral forecast with a velocity view tells you both the timing and the trend, and the dashboards behind it are covered in Monk's piece on cash intelligence dashboards. The practical upside is that finance stops debating which spreadsheet is right and starts asking a better question: which specific invoices are slipping, and what is being done about each one. That shift, from a monthly forecast ritual to a continuous read on cash, is what separates teams that hit their number from teams that explain why they missed it.

Why Does This Matter for the CFO?

Most CFOs do not get burned by revenue surprises; they get burned by cash-timing surprises. You are told collections are on track, you plan against it, and then the wire that was supposed to land this week slips into next month and the whole working-capital plan moves with it. The damage is rarely the amount itself, it is the false confidence the old forecast created.

Grounding forecasts in observable, real-time signals restores that confidence where it matters most: planning headcount, managing working capital tightly, and communicating to a board that expects you to hit your number. The difference shows up in results. Monk customers see a 40%+ reduction in DSO and a 2.4x increase in cash on hand in the first quarter, with one customer growing cash on hand 122% in the first month after going live. Go-live takes one to three days, and Monk takes no percentage of revenue on what it collects, so the economics scale with you rather than against you.

To see a behavior-based motion in practice, read how a fast-growing company rebuilt its collections and forecasting in the Pump case study. For the broader category context, the overview of accounts receivable automation shows where forecasting fits in the wider invoice-to-cash stack.

Frequently Asked Questions

Why are cash flow forecasts usually wrong?

They apply static collection-rate assumptions to aged receivables, ignoring real customer behavior such as payment intent, promises-to-pay, and disputes. Because cash arrives based on behavior rather than due dates, a forecast built only on averages drifts away from reality.

What is behavioral cash forecasting?

It is a forecast built bottom-up from each invoice's live state, payment intent, dispute status, and customer history, rather than from blended historical averages. Each invoice is weighted by its real likelihood and timing of payment.

Why are promises-to-pay so important?

They are the highest-signal indicator of when cash will actually arrive, because they reflect a direct commitment from the customer. Most companies have no system to capture them consistently, so Monk logs them automatically from replies.

How does Monk improve forecast accuracy?

It tracks live invoice state, ingests payment data in real time, captures promises-to-pay, and pauses confidence on disputed invoices until they resolve. The forecast updates continuously instead of being rebuilt by hand each cycle.

How is cash flow velocity related to forecasting?

Velocity measures how fast receivables convert to cash, which is the trend that a behavioral forecast turns into a timing prediction. Tracking both gives finance the rate of conversion and the expected arrival of cash together.

What results do Monk customers see?

A 40%+ reduction in DSO and a 2.4x increase in cash on hand in the first quarter, with one customer reaching 122% more cash on hand in month one. Implementation runs in one to three days.

Ready to forecast on behavior instead of guesswork and turn revenue into cash you can plan around? Book a demo.

.avif)