B2B Debt Collection: The Complete Guide

B2B debt collection is the process of recovering payment on overdue invoices between businesses, and the teams that recover the most treat it as a friction problem rather than a pressure problem. Unlike consumer debt, it involves ongoing relationships, larger invoices, and payment that flows through purchase orders, approvals, and accounts payable portals like Coupa and Ariba. This guide covers how it works, why it differs from consumer collections, the practices that recover more, and how to choose between in-house, an agency, and software.

What is B2B debt collection?

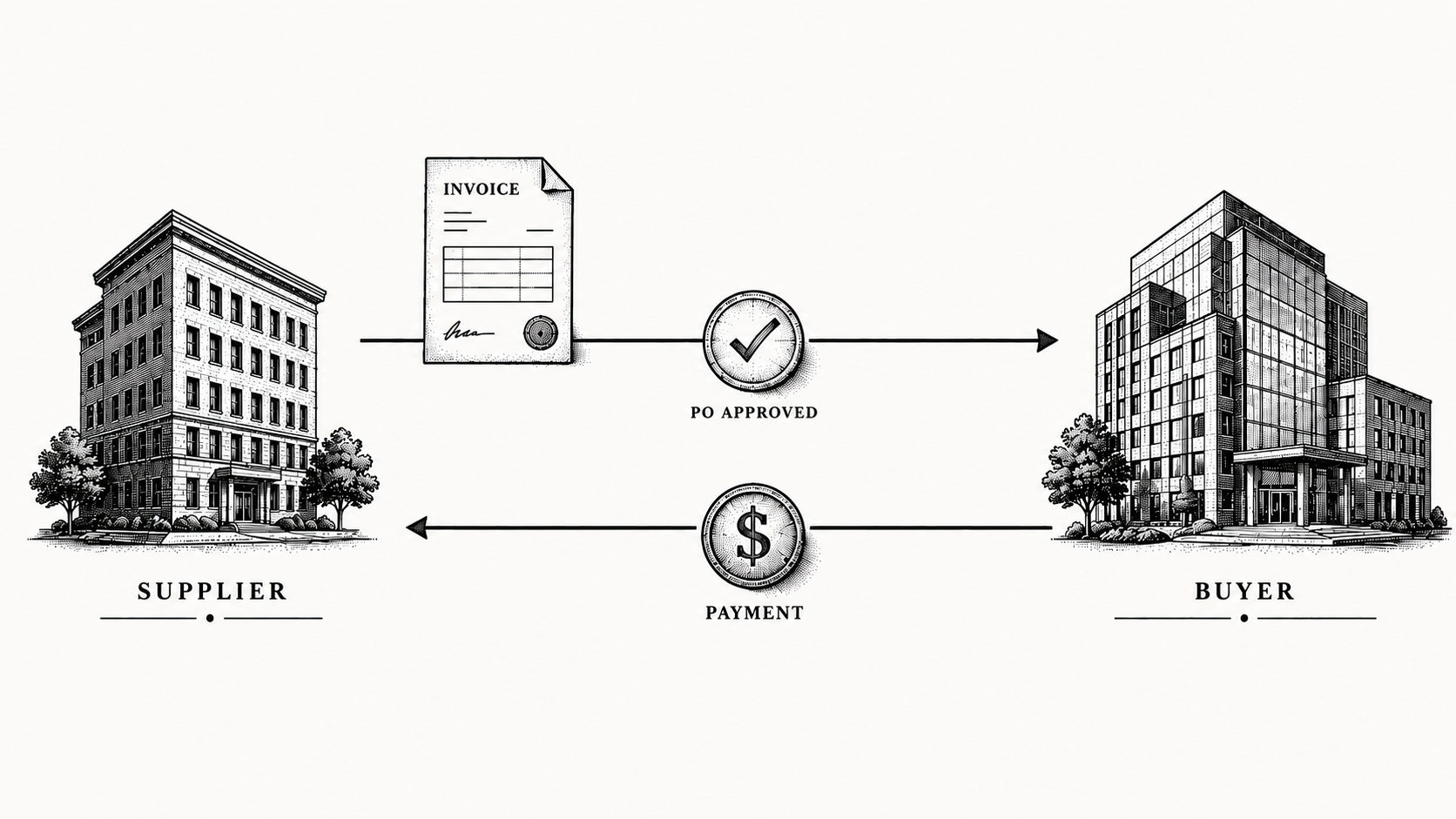

B2B debt collection is recovering what one business owes another on overdue invoices. Because the customer who owes you today is often the renewal you want next year, the goal is to get paid while keeping the relationship intact. That single constraint shapes everything about how good B2B teams operate.

Most B2B late payments are not refusals. They trace to an exception: a dispute, a missing purchase order, an invoice stuck in an accounts payable portal, or a contact who left. That makes B2B collection less about leverage and more about removing whatever is blocking an otherwise willing payer.

How is B2B debt collection different from consumer collections?

Consumer collections are heavily regulated and often adversarial, built around debtors who may never transact with the creditor again. B2B collections are the opposite: relationship-driven, negotiated, and ongoing.

Invoices are larger, terms are agreed in advance, and payment runs through approval chains and portals rather than a single card. The practical implication is that aggressive tactics cost you future revenue, so the right approach protects the relationship while still getting paid.

There is also a timing difference. A consumer balance is often a fixed amount that either gets paid or does not, while a B2B invoice moves through a workflow with several points where it can stall. Knowing where an invoice is in that workflow is usually the key to getting it unstuck.

For example, an invoice may be approved internally by your customer but still waiting on a final sign-off in an accounts payable portal. No amount of pressure on the original contact will move it, because the bottleneck is somewhere else entirely. Tracing the invoice to its actual blocker is what separates effective B2B collections from generic reminders.

What are the best practices for B2B debt collection?

The teams that recover the most follow a consistent playbook rather than improvising per account. Each of the practices below is simple on its own, but the value comes from applying all of them to every account, every time.

Start early

Follow up from the day an invoice is due, not at 90 days. An invoice nudged at day 25 rarely becomes a day-120 problem, and early contact keeps accounts out of the aging buckets entirely. The cost of a polite early reminder is near zero, while the cost of a 120-day account is real.

Stay professional and in your own name

Outreach should sound like you, not a debt collector. Adversarial messaging may extract one payment but costs you the account, which in B2B is far more expensive than the invoice. A professional tone also makes it easier for the customer to raise the real blocker.

Understand why each invoice is unpaid

Before escalating, find the real blocker. A resubmission or an answer moves cash, while a repeated reminder does not. Intent-aware outreach earns about 24% higher response rates than standard dunning, because it responds to what the customer actually said.

Handle AP portals and PO mismatches

Much of the delay in B2B lives in accounts payable portals and in purchase order mismatches. An invoice that is never submitted correctly is never paid, so clearing these is often the whole job rather than a side task.

Offer payment plans before escalating

For strained balances, a structured plan recovers more than waiting for a lump sum, and it keeps the relationship workable. A predictable partial schedule is almost always better than an aging full balance that may never be paid at once. It also signals good faith, which matters when you want to keep doing business with that customer.

Automate the routine

Consistency across every account is impossible by hand at volume. Automation keeps follow-up steady so your team works the genuine exceptions instead of the whole queue, and nothing slips simply because someone was busy that week.

In-house, agency, or software: which should you use?

The right answer depends on the age of the debt and whether you want to keep the customer. The table below maps each option to where it fits best.

| Approach | Best for | Cost | Relationship |

|---|---|---|---|

| In-house team | Lower volume | Salary and time | Preserved |

| Collection agency | Old, written-off debt | 25 to 50 percent fee | Usually lost |

| Collections software | Current and recent accounts | Flat subscription | Preserved |

In-house works until volume outgrows the team. An agency recovers old debt for a steep fee but strains the relationship. Software automates the routine early, keeps the relationship, and prevents most accounts from ever needing an agency, which is why it is the durable answer for growing B2B teams.

These are not mutually exclusive. Many teams run software as their primary engine, keep a small in-house effort for the highest-value exceptions, and reserve an agency strictly for debt they have already written off. The mix shifts as you grow, but the principle holds: automate the routine, work the exceptions by hand, and escalate only what is truly lost.

How do you measure B2B collections performance?

You cannot improve what you do not track, so a few metrics matter more than the rest. Days sales outstanding tells you how long cash sits in receivables, while the share of invoices resolved without escalation tells you how much friction your process removes on its own.

Watching these over time turns collections from a reactive scramble into a managed process. When DSO drops and escalations fall, you are not just collecting faster, you are preventing the problems that create aged debt in the first place.

It also helps to track the most common reasons invoices go unpaid. If disputes drive most of your delays, the fix is earlier dispute handling. If portal rejections dominate, the fix is cleaner submissions. The data tells you where to invest, so you are improving the process rather than working harder on the same broken steps.

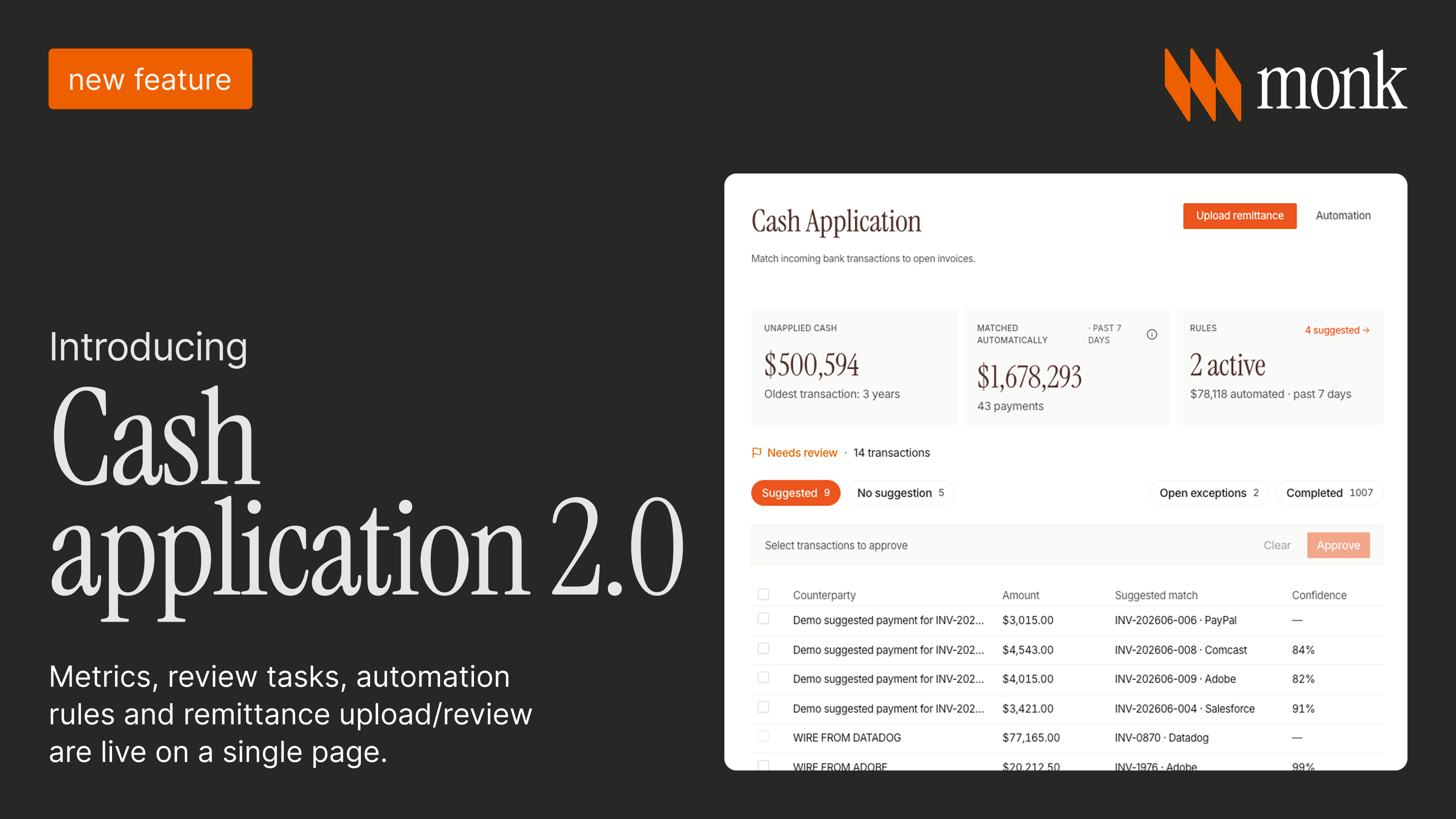

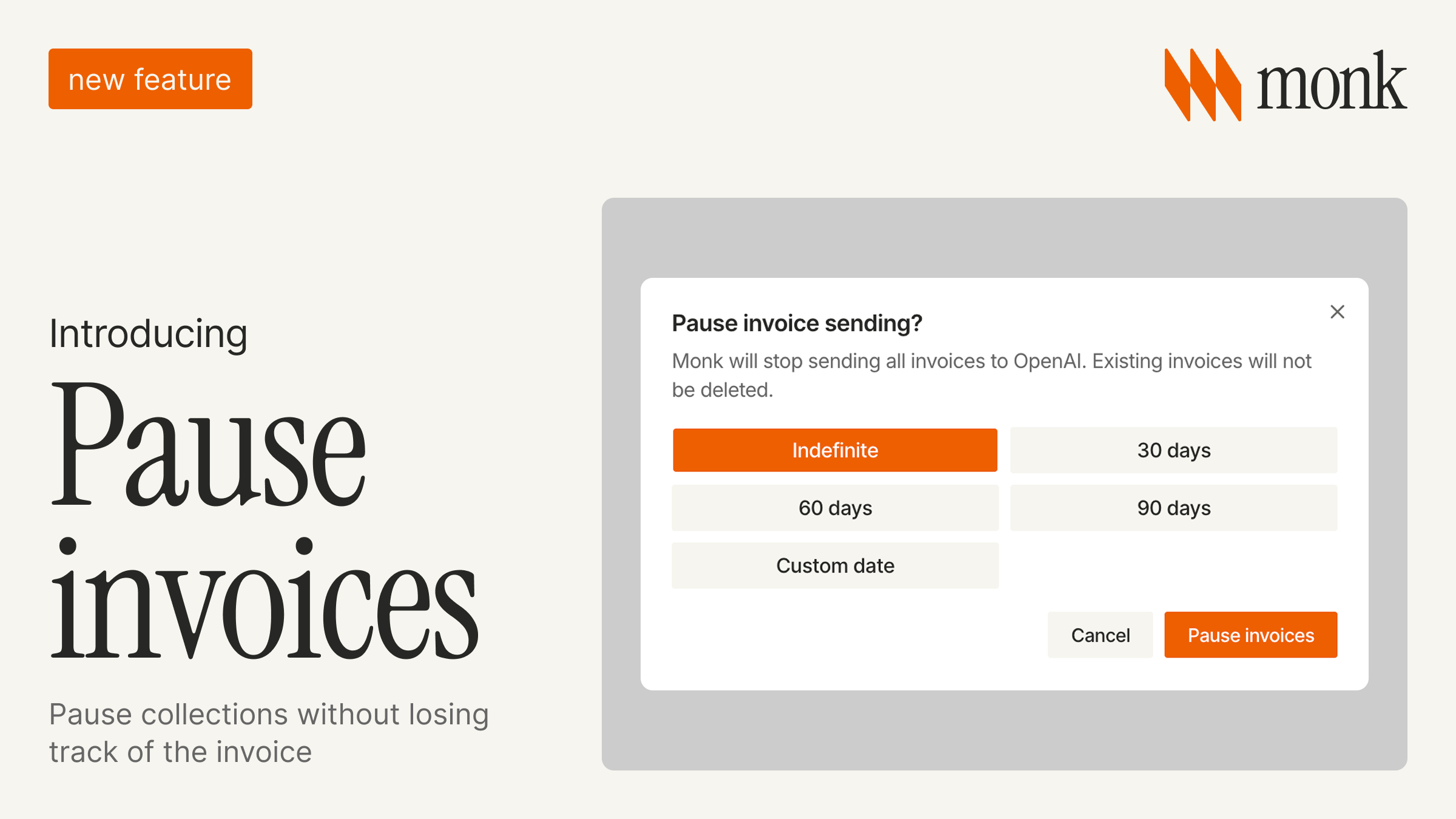

How does Monk run B2B collections?

Monk is an AI-native invoice-to-cash platform built for B2B, with an AR agent named Julia. Its intelligent collections ingest the context of each conversation and respond more effectively than standard dunning, sending personalized follow-ups in your company's name, adapting tone to each customer's history, and applying cash back to your ERP at a 95% match rate.

Customers see a 40% reduction in DSO, save about 26 hours a month, and resolve 88.2% of invoices without escalation, all while keeping every customer relationship intact. Monk integrates with Salesforce, QuickBooks, NetSuite, HubSpot, and Stripe, is SOC 2 compliant, goes live in one to three days, and does not take a percentage of your revenue.

Frequently asked questions

What is B2B debt collection?

It is the process of recovering payment on overdue invoices between businesses, usually involving ongoing relationships, larger invoices, and payment through purchase orders and accounts payable portals.

How is B2B collection different from consumer debt collection?

B2B collections are relationship-driven and less regulated than consumer collections, and most late payments stem from exceptions like disputes or portals rather than refusal to pay.

What is the best way to collect B2B debt?

Start early, stay professional and in your own name, find why each invoice is unpaid, handle accounts payable portals, and automate the routine follow-up so nothing slips.

Should I use software or an agency for B2B collections?

Software is the better fit for current and recent accounts and ongoing relationships. An agency is a last resort for old, likely-uncollectible debt and charges a steep contingency fee.

How long does B2B debt collection take?

It varies by account, but early and consistent follow-up shortens it significantly. On average, Monk customers see a 40% reduction in DSO.

Does collections software hurt customer relationships?

No. Good software sends professional, personalized outreach in your own name and adapts to each customer, which protects the relationship rather than straining it the way a third-party agency can.

.avif)