How to Recover Bad Debt: A Step-by-Step Guide

Bad debt is invoice money that looks unlikely to be collected, often already written down on the books. Some of it is recoverable with a structured process, and some is not, but the largest gain comes from preventing bad debt from forming in the first place. This guide covers how to recover what you can, step by step, and how to stop the next batch from aging that far. Throughout, the goal is to get paid while keeping the customer relationship intact.

What is bad debt, and can you recover it?

Bad debt is the portion of your receivables that has aged to the point where collection is in doubt. Accounting rules push you to reserve against it, but a write-down is not the same as a write-off, and a meaningful share of reserved invoices can still be collected with the right approach.

The honest framing is that recoverability falls fast with age. An invoice 45 days past due is usually a friction problem you can fix, while one 180 days past due with an unresponsive customer is a different and harder situation. The steps below work the recoverable cases hard and escalate the rest cleanly, so you spend effort where it actually returns cash.

How do you recover bad debt, step by step?

Recovery is a sequence, not a single email, and it sits inside a broader B2B debt collection process. Working the steps in order is what separates teams that recover a real share of bad debt from those that send reminders into the void.

1. Prioritize by amount and recoverability

Sort overdue accounts by balance and by how collectible they look, then spend your effort where it pays off. A handful of large, recoverable invoices usually matter more than a long tail of tiny, hopeless ones, and ranking them first keeps your team from burning hours on accounts that will never pay.

2. Confirm why each invoice is unpaid

Many aged invoices are stuck on a dispute, a wrong contact, a missing purchase order, or an unsubmitted invoice in an accounts payable portal like Coupa or Ariba, not an unwillingness to pay. Find the real reason before you escalate, because the fix is often a lookup or a resubmission rather than pressure.

3. Reach out professionally and persistently

Personalized outreach in your own name, adapted to the customer, recovers more than a generic threat. Outreach calibrated to the relationship earns about 24% higher response rates than standard dunning, and it does not burn the account in the process.

4. Offer a payment plan

For larger or strained balances, a structured plan often recovers more than holding out for a lump sum that may never arrive at once. A partial but predictable schedule beats an aging full balance, and it gives a willing-but-stretched customer a realistic path back to current.

5. Escalate only as a last resort

Hand genuinely uncollectible debt to an agency or attorney only after your own outreach is exhausted, knowing that agencies charge a contingency fee of 25 to 50 percent and the relationship rarely survives. Reserve this for accounts you have effectively written off internally.

6. Record the cause and learn

Capture why each account aged into bad debt so you can fix the upstream process and prevent the next one. The pattern usually points back to late or inconsistent follow-up, which is something you can solve systematically rather than account by account. Over a few quarters, those notes become a map of exactly where cash leaks out of your process.

What actually gets bad debt paid?

The common thread across recovered accounts is understanding why an invoice is unpaid and acting on that specific reason, rather than sending another reminder. A lookup, a resubmission, or a direct answer moves cash, while a fourth identical email does not.

Speed matters just as much. The same invoice is far more collectible at day 30 than at day 120, so the highest-leverage move is to work accounts before they ever reach bad-debt status. Recoverability is a function of how fast you act and how precisely you address the blocker.

Consider a common example. A $40,000 invoice sits unpaid at 90 days, and the team assumes the customer is stalling. In practice the invoice was rejected by an accounts payable portal for a purchase order mismatch, and nobody followed up. A single corrected resubmission clears it, while three more reminders would have done nothing. That is the difference between addressing the cause and repeating the symptom.

How do you stop bad debt from forming?

Prevention beats recovery every time, and it is mostly a matter of consistency. Automating early, personalized follow-up, submitting invoices to accounts payable portals, and catching disputes fast keeps accounts from aging into bad debt at all.

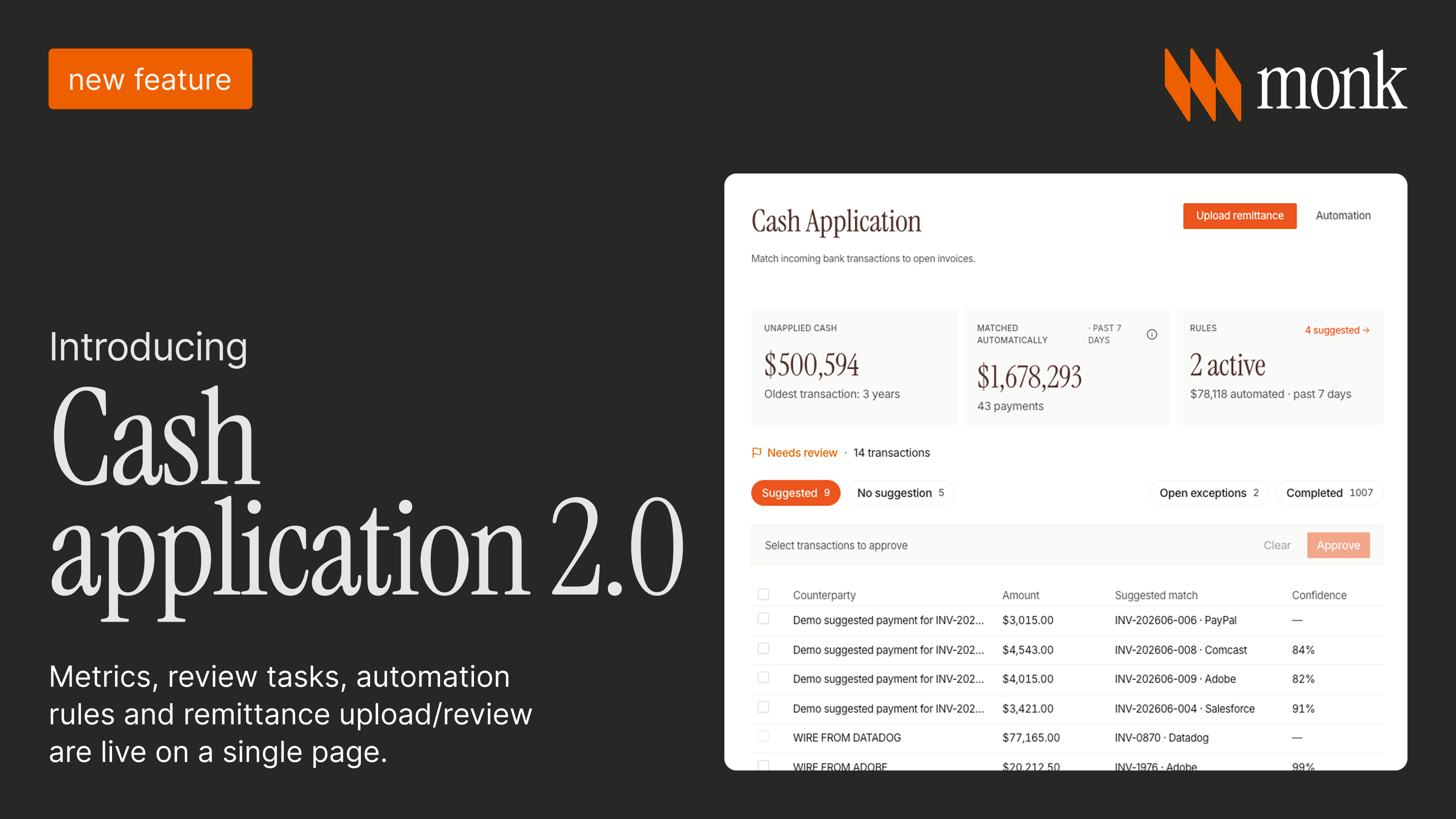

This is where automation changes the math, because it applies that consistency to every account rather than just the largest. Monk customers see a 40% reduction in DSO and resolve 88.2% of invoices without escalation, which means far fewer accounts ever reach the point of being written down.

The practical prevention checklist is short but strict. Send the first reminder on the due date, not weeks later. Verify the contact and purchase order before the invoice ages. Submit to the right accounts payable portal the first time. Flag any dispute the moment it surfaces so it does not quietly sit for a quarter. Done consistently across every account, these habits remove most of the inputs that create bad debt.

Where does software fit against the alternatives?

It helps to see the three common paths side by side, because each fits a different stage of the account.

| Approach | Best for | Cost | Relationship |

|---|---|---|---|

| In-house outreach | Lower volume, recent accounts | Salary and time | Preserved |

| Collections software | Current and recently overdue accounts | Predictable subscription | Preserved |

| Collection agency | Old, written-off debt | 25 to 50 percent contingency fee | Usually lost |

The pattern is clear: software and in-house effort keep the relationship and cost far less, while an agency is a last resort that trades the customer for a chance at old cash. The durable answer for a growing business is to automate early so the agency question rarely comes up. Most accounts that end up at an agency could have been resolved months earlier with consistent, well-timed follow-up that simply never happened.

How does Monk help?

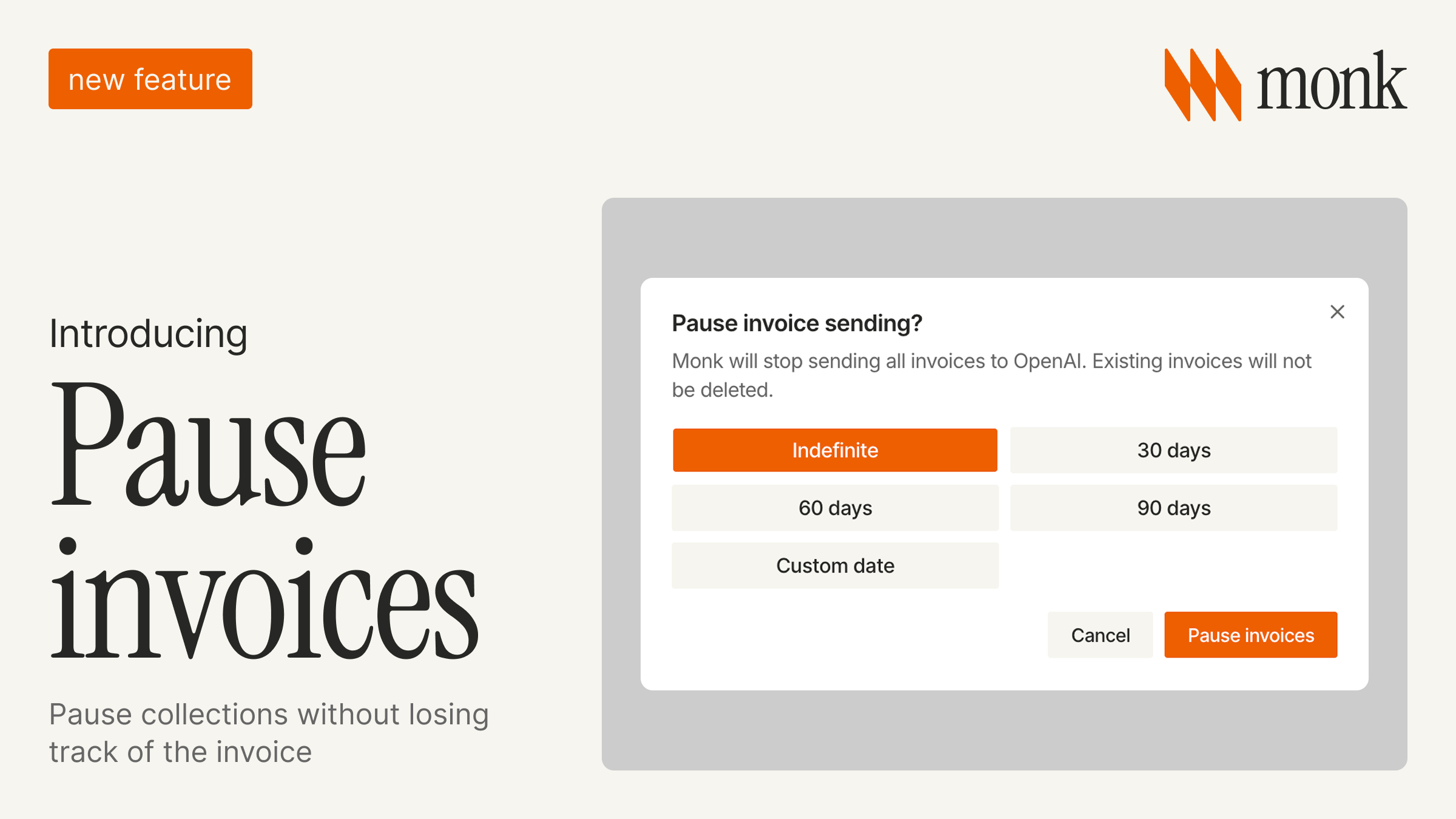

Monk is an AI-native invoice-to-cash platform whose AR agent, Julia, runs intelligent collections that ingest the context of each conversation, respond more effectively than dunning, and apply cash back to your ERP, all in your name. By starting follow-up the day an invoice is due and adapting tone to each customer's history, Monk keeps far more accounts from ever reaching bad-debt territory.

Monk integrates with tools you already use, including Salesforce, QuickBooks, NetSuite, HubSpot, and Stripe, is SOC 2 compliant, and goes live in one to three days. It does not take a percentage of your revenue, so recovery becomes a structured, predictable process rather than an ad hoc scramble after the damage is done.

Frequently asked questions

Can bad debt be recovered?

Some can, especially when follow-up starts early and the real reason for non-payment is addressed. Genuinely uncollectible debt, where the customer is insolvent or gone, is harder and may need an agency.

What is the first step to recovering bad debt?

Prioritize accounts by amount and recoverability, then confirm why each invoice is actually unpaid before escalating. The cause is often a fixable exception rather than a refusal to pay.

When should bad debt go to a collection agency?

As a last resort, for old debt where the customer is unresponsive or insolvent and your own outreach is exhausted. Agencies charge 25 to 50 percent of what they recover.

How do you prevent bad debt?

Automate early, personalized collections, handle accounts payable portals, and catch disputes quickly so invoices never age into bad debt. Consistency from day one is what keeps accounts current.

Does collections software help with bad debt?

Yes. It chases aged invoices and, more importantly, prevents accounts from reaching bad-debt status by keeping follow-up consistent from day one. Monk customers resolve 88.2% of invoices without escalation.

How much faster can automated collections get me paid?

Results vary by business, but Monk customers see a 40% average reduction in DSO and save about 26 hours a month on manual follow-up. Faster, consistent outreach is what keeps invoices from aging into bad debt.

.avif)