Cash Application in SaaS vs. Marketplace Models: A 2026 Playbook

How Does Cash Application Differ Between SaaS and Marketplace Models?

SaaS and marketplace businesses face opposite cash application problems, so the same finance team often needs two different playbooks to keep cash clean. SaaS revenue is recurring and relatively predictable, so the hard part is matching renewals, upgrades, proration, and consolidated payments across many subscriptions. Marketplaces handle high volumes of small, many-to-many payments across buyers and sellers, where the hard part is splitting and attributing each dollar to the right order, seller, and fee. Both models break manual matching, and both inflate days sales outstanding when cash sits unapplied even though the money has already arrived.

This playbook breaks down each model, shows where cash application gets hard, and explains how to automate both without two separate tools. Monk runs AI-native cash application that reads remittance and matches at scale, which is why a single platform can serve recurring SaaS billing and high-volume marketplace flows at once. For the broader context on where this fits, the guide on what accounts receivable automation actually covers is a useful starting point.

What Makes SaaS Cash Application Hard?

SaaS billing is recurring, which sounds simple but creates its own matching problems that get worse as the customer base grows. The structure of subscription revenue, not the volume, is what trips teams up.

A single customer payment may cover multiple subscriptions, a mid-cycle upgrade, or a proration adjustment, and the remittance rarely lines up cleanly with the open invoices. Consolidated payments from a parent entity have to be split across subsidiaries and business units, each with its own invoice numbers and purchase orders. Add in partial payments, short pays, and currency conversions, and a single deposit can require a dozen manual decisions before it clears. When this matching is done by hand, unapplied cash piles up in a suspense account and inflates DSO even though the customer has paid in full.

The fix is matching that reads remittance from the payment itself and handles consolidated and split cases automatically, rather than relying on an analyst to interpret each one. Monk's cash application reaches a 95% match rate, which keeps recurring revenue reconciled and stops paid invoices from being chased in error or sent to collections by mistake. That accuracy also protects the customer relationship, because nothing erodes trust faster than a dunning notice for an invoice that was already paid. If reducing DSO is the priority, the breakdown of six strategies for reducing DSO shows where clean cash application fits in the wider effort.

What Makes Marketplace Cash Application Hard?

Marketplaces invert the SaaS problem entirely. Instead of a few large recurring payments, the challenge is thousands of small transactions that each have to be attributed precisely.

Volume alone makes manual matching impossible to keep up with, and the many-to-many structure compounds it: one settlement file can contain hundreds of payments that must be split across sellers, allocated to specific orders, and netted against platform fees and refunds. A single misattributed payment can ripple into seller payouts and tax reporting, so errors are costly rather than cosmetic. As transaction counts climb, a manual process does not just slow down, it falls behind and never recovers, and the backlog becomes a permanent drag on reporting accuracy.

Marketplaces also deal with payment processors and gateways that report on their own schedules and formats, which means the remittance data arrives fragmented across sources. Stitching that data back together by hand is exactly the kind of repetitive, pattern-heavy work that humans do slowly and machines do instantly. The teams that stay ahead treat reconciliation as a continuous, automated process rather than a periodic cleanup exercise.

The solution is automation that matches at volume and attributes cash to the correct seller, order, and fee line without human intervention. That keeps reconciliation pacing with growth instead of lagging a week or two behind it. The same principle that helps SaaS teams, covered in our look at how remittance matching works, applies directly to marketplace settlement files.

How Do SaaS and Marketplace Cash Application Compare?

The two models share a failure mode, unapplied cash, but reach it from opposite directions. The table below lays out the practical differences a finance leader needs to plan around.

| Dimension | SaaS | Marketplace |

|---|---|---|

| Payment pattern | Recurring, fewer, larger | High-volume, small, many-to-many |

| Main challenge | Consolidated payments and proration across subscriptions | Attribution and splitting at scale |

| Remittance source | Customer emails, parent-entity files | Settlement files, processor reports |

| Failure mode | Unapplied cash inflates DSO | Reconciliation falls behind volume |

| What helps most | Remittance reading, consolidated matching | High-volume automated attribution |

Why Manual Matching Fails in Both Models

Whichever model you run, a manual cash application process carries the same hidden tax: skilled finance staff spend hours keying remittance, hunting for invoice numbers, and clearing suspense accounts. That work scales linearly with growth, so the cost rises exactly when the business can least afford the distraction.

Across our own analysis, a large share of cash-flow slowdowns trace back to predictable, recurring exceptions rather than rare edge cases. In fact, 39% of cash-flow slowdowns are caused by these repeatable exceptions, which is precisely the category automation handles best because the same patterns appear again and again. Teams that automate matching recover real time, with Monk customers saving an average of 26 hours per month that used to go to manual reconciliation.

The cost is not only labor. Every day cash sits unapplied is a day the business cannot see its true collected position, which weakens forecasting and ties up working capital that should be funding growth. Whether the root cause is a consolidated SaaS payment or a fragmented marketplace settlement, the remedy is the same: read the remittance, match it accurately, and post it without waiting on a person to interpret the file.

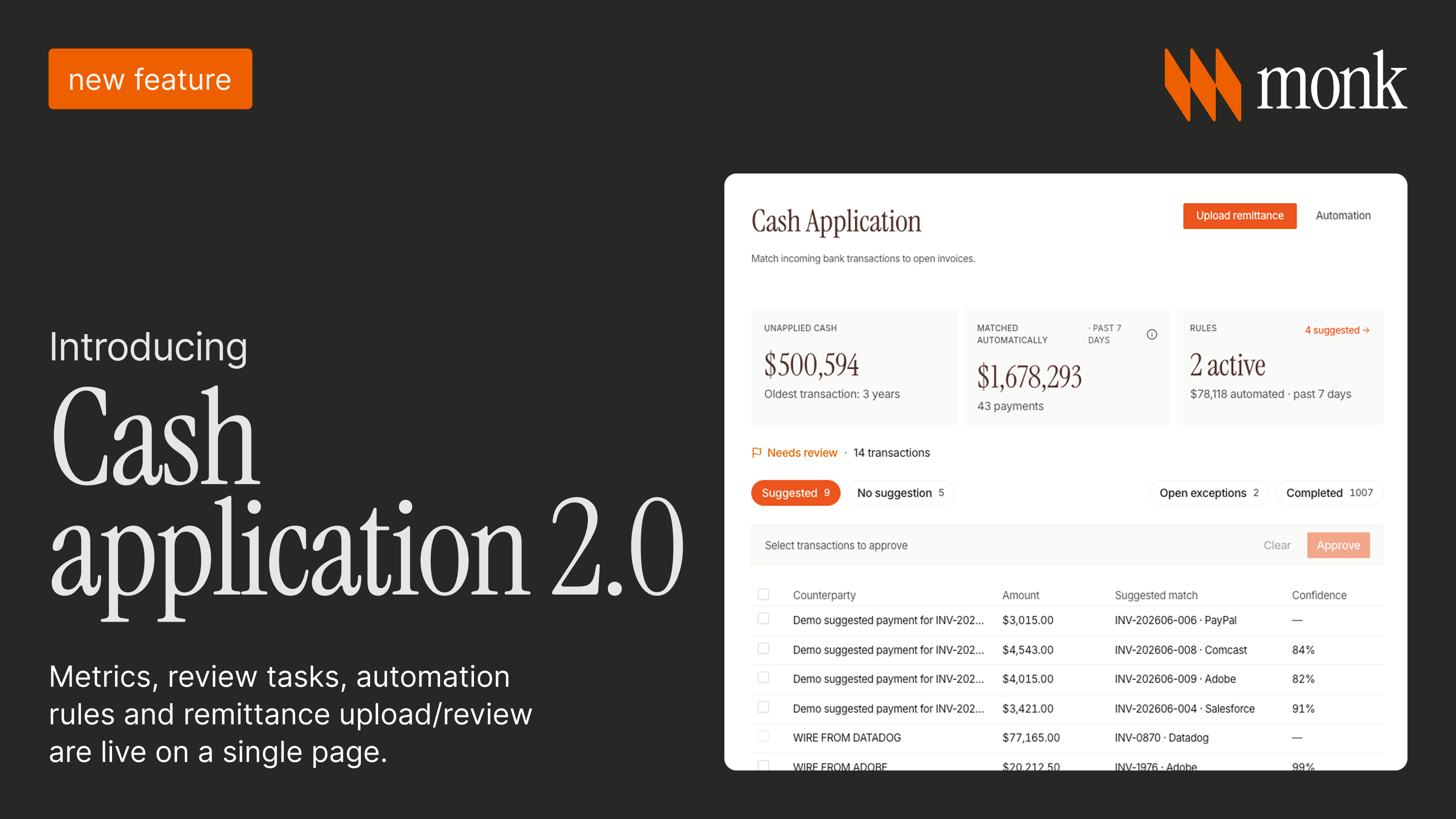

How Does Monk Handle Both Models?

Monk is an AI-native invoice-to-cash platform, and its cash application reads remittance from bank files, customer emails, and AP portals like Coupa and Ariba, then matches each payment to the correct invoices, including split and consolidated cases. That single capability serves both models at once.

For SaaS, it untangles consolidated parent-entity payments and applies proration adjustments without manual splitting. For marketplaces, it attributes high-volume cash precisely across sellers, orders, and fees. Matched cash flows straight into your ERP through native connections to systems like NetSuite, QuickBooks, and Stripe, so reconciliation stays current. Monk reaches a 95% cash application match rate, manages $1.25 billion in AR, and goes live in one to three days, and it does not take a percentage of your revenue. To see how matching connects to collections and the rest of the workflow, explore the AR automation platform and the broader approach in our guide on moving off manual payment matching.

Frequently Asked Questions

Common questions about cash application across SaaS and marketplace business models.

Why does cash application differ by business model?

Payment patterns differ at a structural level. SaaS produces recurring, consolidated payments that span multiple subscriptions, while marketplaces produce high volumes of small, many-to-many payments that each must be attributed to the right seller and order.

What is the hardest part of SaaS cash application?

Matching consolidated and prorated payments across multiple subscriptions, where one payment from a parent entity covers many invoices across subsidiaries. The remittance rarely maps cleanly to open invoices without automated reading.

What is the hardest part of marketplace cash application?

Attributing and splitting high volumes of small payments across buyers, sellers, orders, and fees without falling behind. Volume makes manual matching impossible, and a single error can disrupt seller payouts and tax reporting.

Can one tool handle both SaaS and marketplace cash application?

Yes. AI-native cash application that reads remittance and matches split and consolidated payments serves both models, which is how Monk handles each in one system. The same matching engine untangles SaaS consolidation and marketplace attribution.

How does cash application affect DSO?

Unapplied cash inflates DSO in both models because invoices stay open even after the customer has paid. Automated matching clears cash to the right invoices quickly, which keeps DSO honest; Monk customers see an average 40% reduction.

How quickly can a business automate cash application?

With Monk, go-live typically takes one to three days because it connects to existing ERP and billing systems rather than replacing them. There is no long implementation project before matching begins.

Ready to automate cash application for your model? See how Monk's automation works or book a demo to map it to your billing setup.

.avif)