The Great Unbundling of Finance: Winners, Losers, and the AI Frontier

Prologue: A Cambrian Explosion of Finance Tools

Finance software once meant monolithic ERPs. Oracle, SAP, and Microsoft reigned for decades, bundling ledgers, procurement, and accounts receivable into large suites. Integration effort was the price of compliance. Then SaaS democratized functionality: expense tools, AP automation, cross-border payments, cash-forecasting widgets. Startups unbundled the ERP into a constellation of point solutions optimized for narrow jobs. Over the past decade the average mid-market company saw its finance stack expand from a handful of core platforms to dozens of specialized apps. The point-solution boom created real value, think Bill.com, Coupa, and Brex, but it also birthed complexity. Each new API added friction; every schema mismatch introduced silent errors. Cash cycles slowed, audit headaches multiplied, and CFOs began asking for consolidation. The modern answer is accounts receivable automation built on a single connected data layer.

Now a new force is reshaping the landscape: AI-native orchestration. Large language models parse contracts, invoices, and legal clauses with human-level nuance. Firms like Monk embed agentic workflows that traverse systems, bridging data silos without manual toil. The emergent trend is not another unbundling but a great re-bundling around graph architectures and autonomous agents. This essay charts the trajectory: how we arrived at the explosion, why AI triggers convergence, and what defines winners and losers in the next decade.

First Wave Unbundling: From Mega-Suite to SaaS Mosaic

The first unbundling aligned with cloud economics. Vendors carved out single pain points, such as expense reports and dunning emails, and offered them as sleek web apps. Implementation time dropped, subscription margins rose, and venture capital poured in. Analyst category maps filled with niche segments: AR point solutions, FX hedging platforms, revenue recognition engines. Finance teams gained agility but paid unseen costs in context switching and integration drift. Mid-market finance analysts now spend a meaningful share of every week reconciling data across apps, a hidden tax that crimps cash velocity.

The Ambient AI Tipping Point

Large language models shift the calculus. When a model ingests an invoice rejection email, pulls the portal schema, queries the contract in the graph, and reforms the payload autonomously, the advantage of best-of-breed point tools evaporates. AI levels functional parity but amplifies integration advantages, which is exactly where generative AI actually moves the needle in finance operations. Value gravitates toward whoever owns clean, connected data. A fragmented stack starves agents of context, causing hallucinations and compliance risk. A consolidated, graph-backed platform feeds agents rich relational data, driving speed and trust. The AI tipping point therefore rewards products that orchestrate end-to-end workflows, not isolated features. It is also what lets a platform handle complex payment terms without snapping back to manual work.

Winners: Platforms with Graph DNA and Agentic Layers

The new champions share traits. They anchor on a schema-flexible graph, ingesting contracts, invoices, payments, and engagement events. They expose retrieval APIs optimized for LLM context windows, minimizing token waste while maximizing ground-truth recall. Their policy engines encode credit rules and escalation logic as code, enabling safe autonomy. They treat integrations as first-class citizens, version-controlled and observable. And they monetize on outcomes, such as DSO reduction and working-capital improvement, rather than seat licenses.

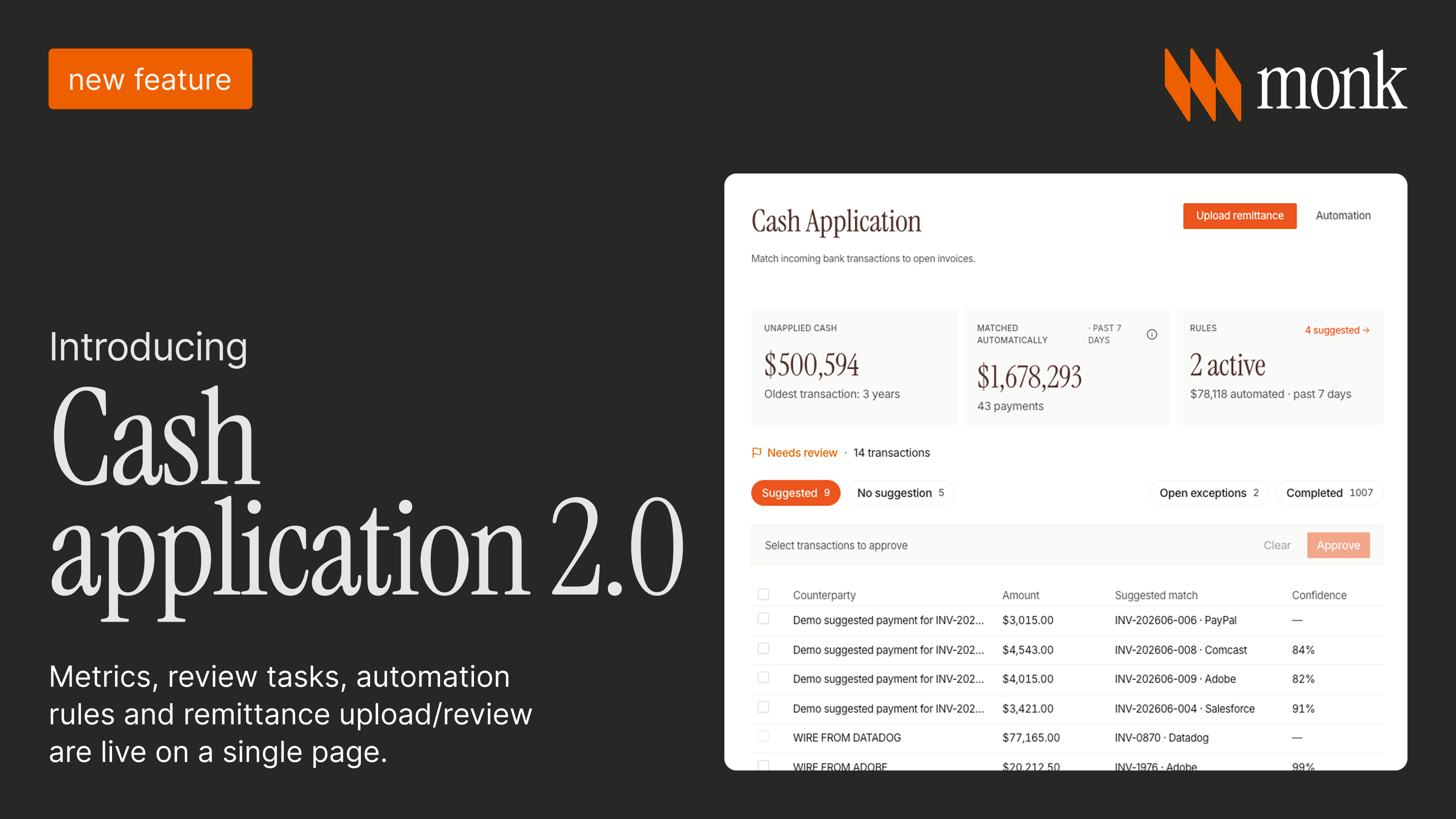

Monk exemplifies the model. By unifying contract-to-cash in a single graph and layering autonomous agents, Monk delivers a 40% average reduction in DSO and manages $1.25B in AR under management. Profound, after consolidating its AR onto Monk, grew its cash on hand 122% in the first month and cut its aging balance fivefold. Clients retire several point solutions, collapsing cost while boosting control. The platform logs every agent decision, satisfying auditors who once distrusted AI. In effect, Monk re-bundles AR around a data substrate fit for AI, flipping fragmentation from liability to moat. That substrate is the contract-to-cash graph at the center of the architecture.

Losers: Feature Islands and Middleware Relics

Point solutions that cling to narrow scope without owning critical integrations face a squeeze. As AI commoditizes feature depth, their differentiation shrinks. Without proprietary data graphs they rely on brittle API calls to gather context, undermining agent reliability. Middleware vendors that brokered integrations risk obsolescence as platforms internalize connectors. Even mega-suite incumbents face pressure if their monolith schemas resist graph transformation; bolting a chat copilot onto decades-old tables cannot match a native event-sourced ledger.

Investor indicators reflect the shift. Valuation multiples for workflow SaaS with sub-category niches have compressed sharply over recent years. Meanwhile, AI-orchestrated finance platforms with graph backbones still command stronger multiples. Talent migration follows capital; engineers move from rule-based vendors to build policy-as-code runtimes at AI-native companies.

Strategic Playbook: Thrive in the Unbundled and Rebundled Future

Own Your Data Graph. Centralize contract, usage, and payment events in a schema-flexible store. Resist quick wins that duplicate data outside the graph; duplication breeds drift.

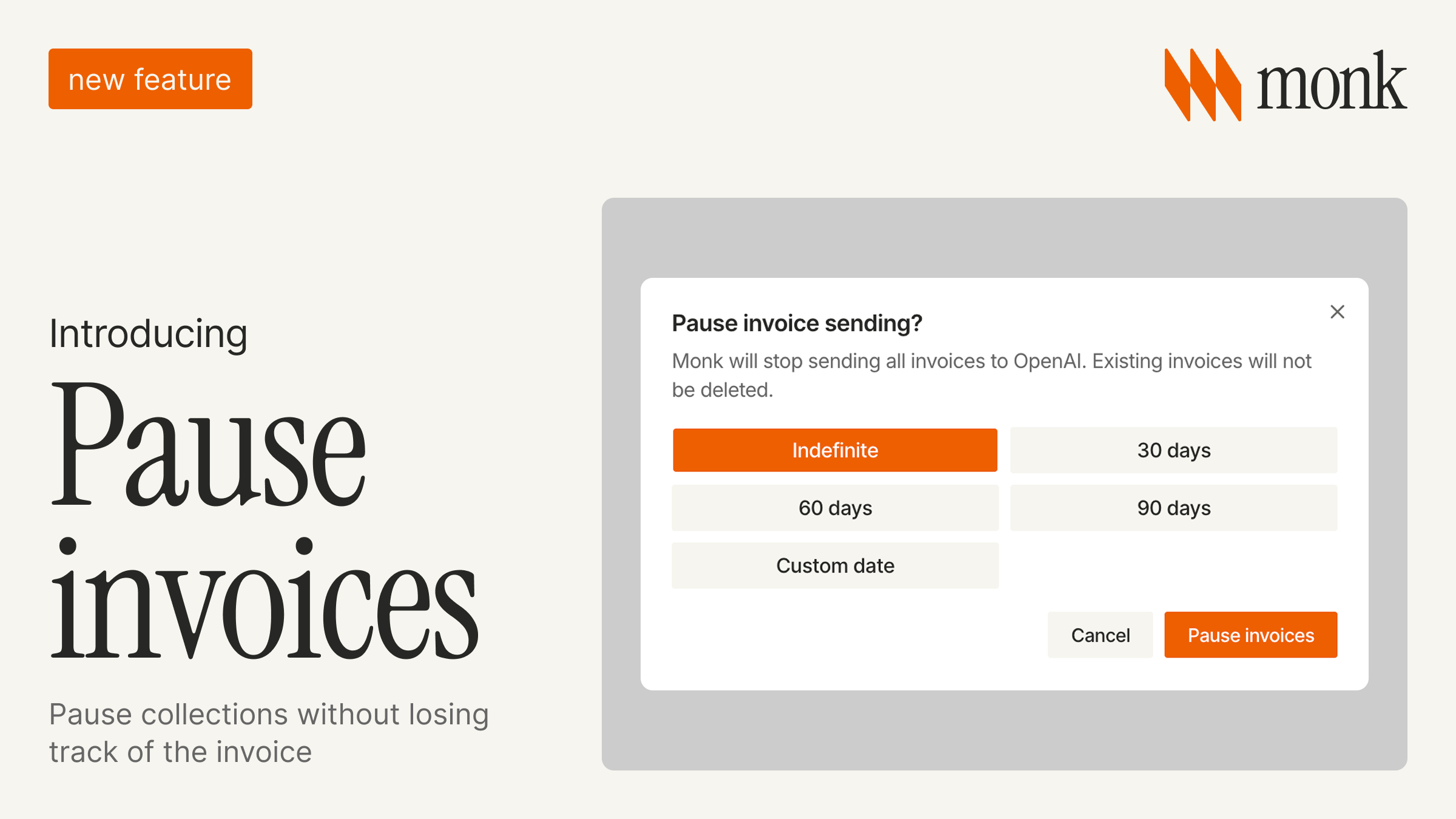

Prioritize Outcomes over UI Features. Customers buy faster cash, the kind that compresses contract-to-cash to days, not prettier dashboards. Build metrics that tie usage to DSO reduction and present ROI proof. Monk's invoice-to-cash platform is organized around exactly that outcome.

Design for LLM Retrieval. Expose narrow, idempotent endpoints returning JSON with crisp names. Assume tokens cost money; retrieval beats generation.

Embed Policy Guardrails. Autonomous agents must obey credit limits and tone guidance. Express rules as version-controlled code; surface diff logs for auditors.

Market AI as Infrastructure, Not Flash. Hype fatigue is real. Show chain-of-thought audit logs and tangible cash gains. CIOs trust controlled transparency.

Bet on Platform Partnerships. Integrate deeply with ERPs and CRMs; expose early-access APIs. When consolidation accelerates, being the preferred AI orchestrator inside a major ecosystem outlasts standalone positioning.

Regulatory Horizon: AI Assurance Frameworks

As AI orchestrates financial flows, regulators tighten oversight. The EU's AI Act mandates risk assessments and human-in-the-loop review for critical finance decisions. US regulators are examining autonomous credit judgments. Platforms win by embedding compliance in policy engines: role-based approvals, audit logs stapled to every agent action, and fail-open modes that hand off to humans upon anomaly detection. Monk invested early in SOC 2 compliance and data masking, giving prospects a compliance runway competitors scramble to match.

Case Vignettes: Winners, Flounders, and Pivots

Winner: an illustrative logistics scale-up. A fast-growing logistics company consolidates several finance tools into one graph-backed platform. DSO falls meaningfully, and the freed cash funds expansion. The controller cites graph lineage as the decisive feature: agents do not hallucinate when every data point has provenance.

Flounder: a niche tax-calculation tool. A single-purpose tax SaaS loses ground after larger platforms embed AI tax modules. Without proprietary graph data, its rates become commodity.

Pivot: a former integration broker. A middleware vendor reinvents itself as a context provider, offering a graph overlay and an LLM retrieval API and partnering with platforms. The lesson is that middleware can survive by evolving into a context layer rather than remaining plumbing.

Predicting the Next Five Years

- Platforms Solidify. A few players dominate AR orchestration, each offering graph plus agents plus compliance.

- ERP Graphification. Incumbents retrofit event stores and may acquire graph natives to skip years of refactoring.

- Agent-to-Agent Protocols. Buyer and supplier agents coordinate terms in real time, rendering static net terms obsolete.

- Treasury Convergence. Graphs extend to bank APIs; cash management workflows sweep funds based on predictive DSO curves.

- AI Audit Markets. Third-party firms certify agent decisions, selling assurance much as certificate authorities sell trust today.

Epilogue: Choose Your Bundle Wisely

Finance unbundled to escape ERP rigidity, but fragmentation birthed new pain. AI now offers a route to reunion, an intelligent bundle centered on data graphs and autonomous agents. Winners will own end-to-end context, deliver cash outcomes, and bake compliance into code. Losers will cling to feature islands as the tide rises. Monk stands among the builders of this new bundle, proving that when context and autonomy converge, the finance stack becomes a growth engine, not just a ledger.

| Era | What it looked like |

|---|---|

| Bundled ERP | Monolithic suites from Oracle, SAP, and Microsoft bundled ledgers, procurement, and accounts receivable. Compliance came at the cost of heavy integration effort. |

| Unbundled point tools | SaaS broke the ERP into a constellation of narrow apps for expense, AP, FX, and forecasting. Agility rose, but reconciliation overhead and integration drift grew with the stack. |

| AI-native re-bundling | Schema-flexible graphs and autonomous agents reunite the stack around clean, connected data, monetizing on outcomes such as DSO reduction rather than feature breadth. |

The great unbundling is not a story of disintegration but of recomposition. The question for every finance leader and software builder is simple: when the pieces come back together around AI, will you control the bundle or compete on its periphery?

Frequently asked questions

What is the great unbundling of finance?

The great unbundling of finance refers to the shift from monolithic ERP suites to a constellation of specialized SaaS point solutions for tasks like expense management, AP automation, and cash forecasting. It delivered agility but also added integration friction, schema mismatches, and reconciliation overhead.

Why is AI driving a re-bundling of the finance stack?

Large language models can parse invoices, contracts, and portal schemas and act across systems, so the advantage of isolated best-of-breed tools fades. Value shifts toward platforms that own clean, connected data, because a fragmented stack starves agents of context while a graph-backed platform feeds them rich relational data.

What traits define the winners in this shift?

Winning platforms anchor on a schema-flexible graph that ingests contracts, invoices, payments, and engagement events. They expose retrieval APIs tuned for LLM context, encode credit and escalation rules as version-controlled policy code, treat integrations as first-class citizens, and monetize on outcomes like DSO reduction.

Which finance tools are most at risk?

Narrow point solutions that do not own critical integrations face a squeeze as AI commoditizes feature depth, and middleware vendors that brokered integrations risk obsolescence as platforms internalize connectors. Mega-suite incumbents also struggle if their schemas resist graph transformation.

How does Monk fit into the re-bundling trend?

Monk unifies invoice-to-cash in a single graph and layers autonomous agents on top, letting clients retire several point solutions while keeping control. Every agent decision is logged for auditability, turning what was once fragmentation into a connected data substrate built for AI.

.avif)