DSO Calculator and Formula Guide

Days Sales Outstanding (DSO) is the average number of days it takes your business to collect cash after making a credit sale. You calculate it with one core formula: DSO = (Accounts Receivable / Total Credit Sales) x Number of Days. A DSO calculator simply automates that math so you can track collection speed over time and spot trouble early. This guide walks through the formula, a worked example, and how to read your result accurately without misleading yourself or chasing the wrong problem.

DSO is one of the most watched metrics in finance because it converts a messy receivables ledger into a single, comparable number. Whether you run it by hand, in a spreadsheet, or through a calculator, the inputs and the interpretation are the same. The sections below cover each input, a step-by-step example, and the common mistakes that produce a misleading figure.

It also helps to keep in mind what DSO is not. It is not a measure of profitability, and it does not tell you whether a specific customer is late; it is a portfolio-level average of how quickly your sales turn into cash. Used that way, alongside an aging report that shows where the balance actually sits, it becomes one of the clearest early signals of how your collections process is performing.

What Is the DSO Formula?

The DSO formula expresses how long, on average, your receivables stay unpaid. The standard version is:

DSO = (Accounts Receivable / Total Credit Sales) x Number of Days

Each input matters. Accounts receivable is the balance customers owe you at the end of the period. Total credit sales is revenue billed on credit during that same period, excluding cash sales. Number of days is the length of the period you are measuring, typically 30, 90, or 365. For a deeper conceptual breakdown, see Monk's explainer on what DSO means in finance.

The logic behind the formula is simple once you see it. Dividing receivables by credit sales tells you what fraction of a period's sales is still sitting unpaid; multiplying by the number of days in that period translates that fraction into a number of days. The result is an average, so it blends fast-paying and slow-paying customers into one figure, which is why it works best as a directional indicator rather than a precise statement about any single invoice.

How Do You Use a DSO Calculator?

A DSO calculator takes the same three inputs and returns your result instantly. Enter your ending accounts receivable balance, your total credit sales for the period, and the number of days in that period. The tool divides receivables by credit sales and multiplies by the day count. The benefit is consistency: you remove manual errors and can recompute the moment new data lands.

The real value of a calculator is not the single answer but the ability to run scenarios. You can test what your DSO would look like if you collected a large overdue invoice, or model the effect of tightening terms, in seconds rather than rebuilding a spreadsheet each time. For a step-by-step manual walkthrough you can follow alongside the tool, read Monk's guide on how to calculate DSO.

What Is a Worked DSO Example?

Suppose a company finishes a 90-day quarter with $450,000 in accounts receivable and $1,500,000 in total credit sales. The table below shows the calculation.

| Input | Value |

|---|---|

| Accounts Receivable | $450,000 |

| Total Credit Sales | $1,500,000 |

| Number of Days | 90 |

| Calculation | (450,000 / 1,500,000) x 90 |

| DSO Result | 27 days |

In this illustrative example, it takes about 27 days on average to collect after a sale. These figures are purely for demonstration and are not industry benchmarks. To judge whether 27 days is good for that business, you would compare it against the company's own payment terms, as explained in Monk's overview of what counts as a good DSO.

Which Inputs Affect Your DSO?

Three levers move your DSO. First, the receivables balance: the more unpaid invoices you carry, the higher the number. Second, credit sales volume: higher sales relative to outstanding balances pull DSO down. Third, the period length: comparing a monthly DSO to an annual one without adjusting the day count produces nonsense. Always match the day count to the period you measured, and use credit sales rather than total sales to avoid understating the figure, since cash sales were never outstanding as receivables and including them inflates the denominator and reports a faster collection cycle than the business actually achieved.

A subtle trap is the choice of receivables balance. Using the period-end balance is standard, but if your sales are seasonal or lumpy, a single snapshot can distort the result. Some teams use an average of the opening and closing balance to smooth this out, which is worth doing whenever a quarter ends on an unusually high or low receivables day.

One more nuance is worth flagging: the day count and the sales figure must cover the same window. If you measure receivables at quarter end, your credit sales input should be the credit sales for that quarter, paired with a 90-day count. Mixing a year of sales with a 90-day count, or vice versa, is the most common way teams accidentally produce a DSO that is off by a factor of three or four and then chase a problem that does not exist.

How Should You Interpret Your DSO Result?

DSO is most useful as a trend, not a single snapshot. Track it month over month and compare it to your own payment terms. If you offer net-30 terms and your DSO sits well above 30, customers are paying late and cash is trapped in receivables. A rising trend signals weakening collections or looser credit policy, while a falling trend usually reflects faster cash conversion.

Always compare against your own terms and history before drawing conclusions, and avoid reading too much into any single month. A large invoice paid or issued near the period boundary can swing the number temporarily, which is why the direction of travel matters more than one reading. For the strategies that actually move the number, Monk's guide on how to reduce DSO lays out a practical playbook.

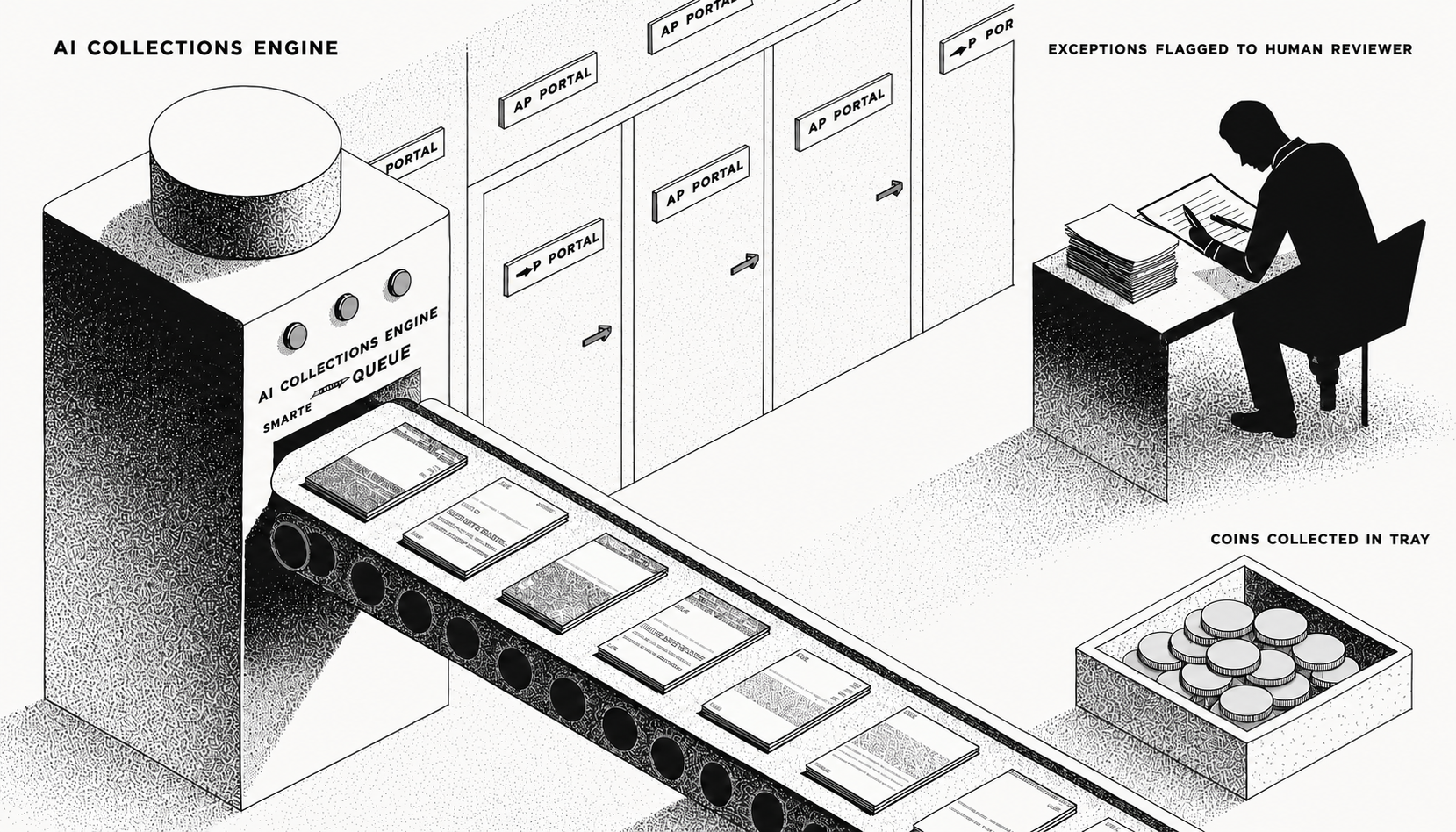

How Can You Improve a High DSO?

If your calculator returns a number higher than you want, the fix is faster, more consistent collections. Monk is an AI-native invoice-to-cash platform that helps teams collect sooner: customers using Monk have seen DSO reductions of 40 percent or more, collections that are 24 percent more effective than traditional dunning, and 90 percent of invoices resolved without escalation. Teams also recover roughly 26 hours per month of manual follow-up work.

The mechanism is straightforward. Monk's intelligent collections ingests the context of each customer conversation and tailors the follow-up, so reminders land at the right time in the right tone instead of as identical dunning. Faster, more responsive collection directly lowers the receivables balance in your DSO formula, which is the single input most within your control. Because Monk also handles invoicing and cash application in the same platform, the receivables figure feeding your DSO stays clean and current.

Frequently Asked Questions

What is the basic DSO formula?

The formula is DSO = (Accounts Receivable / Total Credit Sales) x Number of Days. It returns the average number of days to collect cash after a credit sale.

Should I use total sales or credit sales in the formula?

Use total credit sales. Including cash sales understates DSO because those amounts were never outstanding as receivables.

What number of days should I use?

Match the day count to your measurement period: 30 for a month, 90 for a quarter, or 365 for a year.

Is a lower DSO always better?

Generally yes, since lower DSO means faster cash collection, but compare it against your own payment terms and history rather than an arbitrary target.

How often should I calculate DSO?

Most teams track DSO monthly so they can spot trends early and act before cash gets stuck in aging receivables.

Should I use the ending or average receivables balance?

The ending balance is standard, but if your sales are seasonal or lumpy, averaging the opening and closing balance gives a more representative result.

Book a demo to see how Monk automates collections and lowers DSO, or explore the full picture in Monk's complete AR automation guide.

.png)

.avif)