One-Day Cash Application: Automating Remittance Matching for 2026

What Is One-Day Cash Application?

One-day cash application means matching incoming payments to invoices and posting them within a day of receipt, instead of letting cash sit unapplied for days while someone hunts down remittance details. It closes the gap between money landing in your bank and that money showing up as recognized, applied cash on the ledger. Achieving it depends on AI-native remittance matching, because the delay is almost always caused by messy payment data that rules-based tools cannot read. The goal is not speed for its own sake; it is an accurate, current picture of what you have actually collected.

This explainer covers why cash sits unapplied, how automated remittance matching closes the gap, and what changes once posting happens within a day. Monk runs this process with AI-native cash application that reaches a 95% match rate, which is why one-day posting is realistic rather than aspirational. For the wider picture of how this fits into receivables, our overview of what accounts receivable automation covers is a good place to start.

Why Does Cash Sit Unapplied for Days?

Cash sits unapplied because payments and their remittance rarely arrive together or cleanly. The bank tells you money came in; it does not tell you which invoices it pays.

A bank file lists deposits, but the invoice references live in a separate email, a PDF attachment, or a truncated bank memo that cuts off the reference number. Customers also pay in their own formats and on their own schedules, so no two remittances look quite alike. Someone has to reconnect the two by hand, and the problem multiplies with consolidated payers who remit one lump sum across dozens of invoices net of credits, marketplace payouts net of fees, and multi-currency wires. Rules-based matching breaks on all of these, so the cash lands in a suspense account and waits for a person to investigate. This is also the core limitation of the traditional bank-driven model, as our comparison of lockbox versus modern cash application explains in detail.

That waiting is where the days accumulate. A payment received Monday might not be applied until Thursday or the following week, depending on the analyst's queue and how many ambiguous files are ahead of it. During busy periods such as quarter-end, the backlog grows fastest precisely when accurate cash visibility matters most. Our analysis found that 39% of cash-flow slowdowns are caused by predictable, recurring exceptions, and unapplied cash is one of the clearest examples of that pattern, because the same difficult remittance formats reappear month after month.

Why Does Unapplied Cash Matter?

Unapplied cash is money you have already received but cannot yet see or use. It is a reporting problem that quietly becomes an operational one.

It inflates DSO because received payments still show as outstanding, it distorts the cash forecast that finance relies on for planning, and it triggers collections outreach on invoices that are actually paid. That last point is the most damaging in practice, because nothing erodes a customer relationship faster than a reminder for a bill they already settled. The longer cash sits in suspense, the more these problems compound across every downstream report and conversation.

There is a working-capital dimension too. Cash that is received but not yet recognized cannot be confidently deployed, so the business effectively underuses money it already holds. For finance leaders, the connection between unapplied cash and elevated DSO is direct, which is why the topic appears prominently in our guide to reducing DSO.

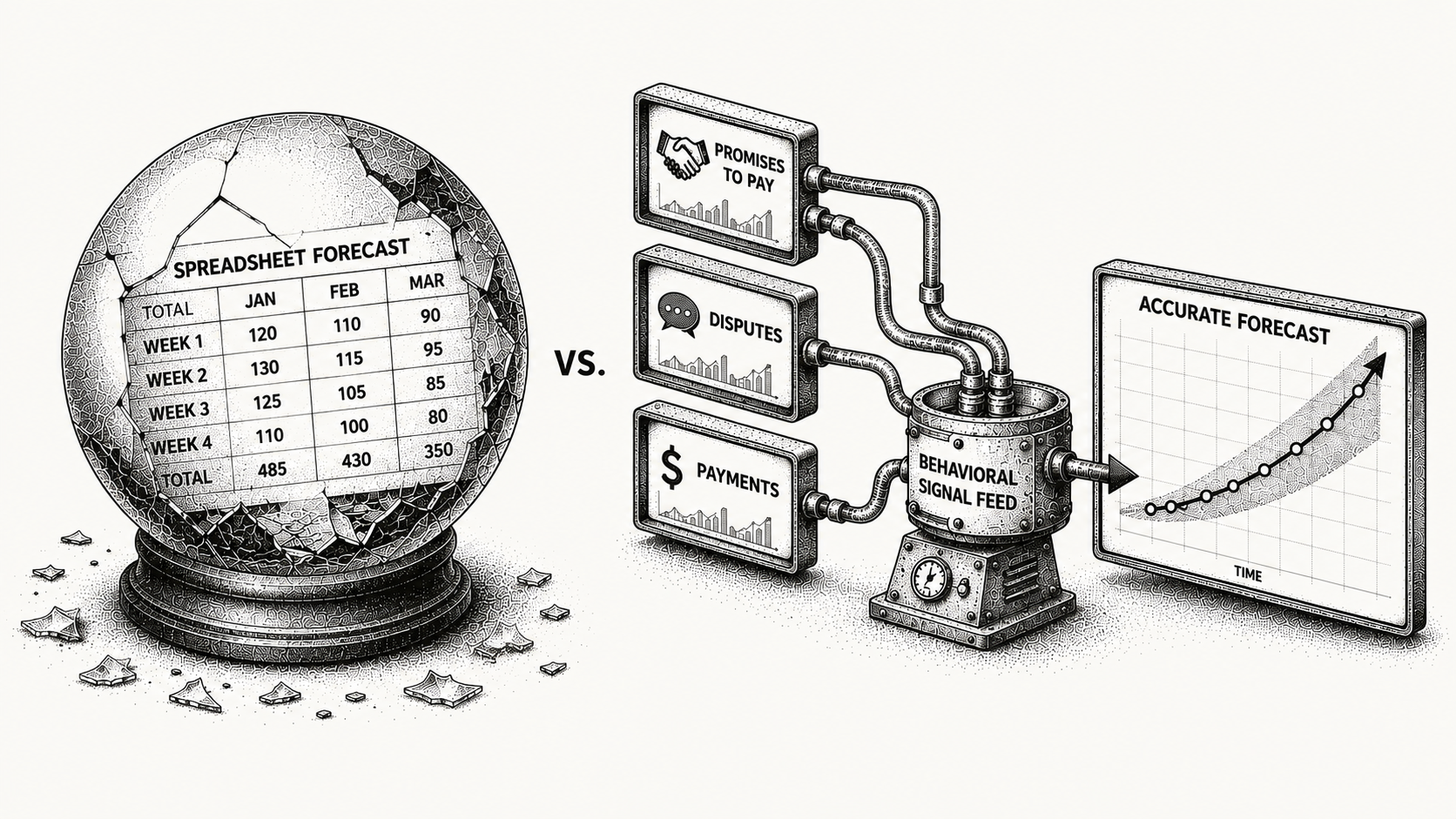

How Does AI-Native Remittance Matching Work?

AI-native cash application reads unstructured remittance from bank files, customer emails, and AP portals like Coupa and Ariba, interprets the references, and matches each payment to the correct open invoices. It handles partial payments, short-pays, and deductions, along with consolidated and multi-currency cases that defeat a fixed rules engine.

High-confidence matches post automatically, and only genuine exceptions route to a person for a quick review. The difference from older tools is that the system reads the actual context of each remittance rather than depending on rigid rules that fail the moment a format changes. A consolidated payment covering fifteen invoices net of two credit memos is a routine case for this approach and a stall point for a rules engine.

Monk does exactly this, applying the matches it is confident in and flagging the rest, and posted cash flows into your ERP through native integrations with systems like NetSuite, QuickBooks, and Stripe. Because matching and collections share the same underlying data, applied cash immediately suppresses any follow-up on invoices that are now paid, which is what protects the customer experience. Profound saw this directly, growing cash-on-hand 122% in its first month with Monk after automating submissions to Coupa, Ariba, and 11 Fortune 500 AP portals, as detailed in the Profound case study. The underlying mechanics are covered in more depth in our explainer on how remittance matching works.

How Does One-Day Posting Compare to the Manual Cycle?

The contrast between a manual cycle and one-day posting is stark across every dimension that matters to finance. The table below lays it out.

| Dimension | Manual cycle | One-day with Monk |

|---|---|---|

| Remittance handling | Hunted across email and portals | Read automatically across channels |

| Consolidated and net payments | Reconstructed by hand | Matched automatically |

| Time to apply | Days, in suspense | Within a day |

| DSO impact | Inflated by unapplied cash | Reflects reality |

| Team focus | Every payment | Only true exceptions |

What Changes Once You Post Cash in a Day?

When posting happens within a day, the suspense account stays near zero and the entire downstream picture clears up. The change is felt well beyond the AR team.

DSO reflects real collection rather than a backlog, the cash forecast becomes trustworthy, and collections stops chasing already-paid invoices. Month-end close speeds up because there is no payment backlog to clear at the deadline, and the finance leader gets a clean, current view of collected cash for working-capital decisions. The AR team's role shifts from data entry to judgment, since the only work left is the small set of genuine exceptions that need a human eye. Monk customers save an average of 26 hours per month and see 88.2% of invoices resolved without escalation as part of broader contract-to-cash automation. Because Monk goes live in one to three days and does not take a percentage of revenue, the path to one-day posting is short and the economics stay simple. You can see how matching connects to the rest of the workflow on the AR automation platform, and the related discipline of clearing the backlog itself is covered in our guide to moving off manual payment matching.

Frequently Asked Questions

Common questions about one-day cash application and automated remittance matching.

What is one-day cash application?

It is matching and posting payments within a day of receipt, rather than leaving them unapplied while remittance is tracked down by hand. The result is a ledger that reflects what you have actually collected, in near real time.

Why does cash end up unapplied?

Remittance often arrives separately from the payment or with unclear references, and consolidated or net payments break rules-based matching. The cash then lands in a suspense account and waits for manual investigation.

How does AI improve remittance matching?

It reads unstructured remittance from bank files, emails, and AP portals and matches partial, consolidated, and multi-currency payments that rules-based tools cannot. It posts the confident matches automatically and flags only genuine exceptions for review.

How does unapplied cash affect DSO?

Received-but-unapplied payments still show as outstanding, inflating DSO and distorting the cash forecast until they are posted. Applying cash quickly keeps DSO honest and the forecast reliable.

Does one-day cash application require replacing my ERP?

No. AI-native cash application integrates with your existing ERP and posts matched cash back automatically, so the ledger remains your system of record. With Monk, that connection is typically live in one to three days.

How quickly can a team reach one-day posting?

Because Monk connects to existing bank, billing, and ERP systems rather than replacing them, go-live takes one to three days. Unapplied cash usually begins falling within the first reconciliation cycle after that.

What kinds of payments are hardest to apply within a day?

Consolidated payments netted against credits, marketplace payouts netted against fees, and multi-currency wires are the usual culprits, because their remittance is fragmented and nonstandard. AI-native matching handles these automatically, which is what makes one-day posting achievable across the whole payment mix rather than just the easy cases.

Want to apply cash within a day? See how Monk automates remittance matching or book a demo to map it to your systems.

.avif)